JFK to 911 Everything Is A Rich Man's Trick

Published on Nov 19, 2014

The who, how & why of the JFK assassination. Taken from an historical perspective starting around world war 1 leading to present day. We hope after watching this video you will know more about what happened in the past and how the world is run today.

All Wars Are Banker Wars, All Bank Owners are Jews

Published on Feb 4, 2013

Written and spoken by Michael Rivero. A video by Zane Henry Productions we made a new version of ‘All Wars Are Banker Wars, All Bank Owners are Jews’ Wars’ that contains a lot of new animations.

Download All Wars Are Banker Wars, All Bank Owners are Jews PDF copy

The artist against the system down through time

- By Jon Rappoport - December 24, 2012

Whatever his medium, the artist stands outside the group and group’s slogans.

If the group is living in Tuesday, he is living in Friday.

He sees invention everywhere, even in the faces that float by on the street. He sees their theatrical roles and the messages that are written on their lips before they speak.

He sees the preposterous crises that are concocted to lead to revelations that never come. Populations walk through one gate after another, deeper into an internal slavery that knows no limit.

The artist sees one genuine emotion after another parlayed into flashes of cheap sentiment.

In midst of all this, the artist doesn’t surrender. Nor does he only observe. Nor does he only point out the lies.

He CREATES.

He always has.

The artist opposes the most popular trends of the moment.

The trend now, under various guises, is the Collective.

We need to realize that the Collective, no matter how it is defined or shaped or covertly hidden, is seeking to marginalize the person who imagines and creates new realities.

The artist is able to spot the Collective. He opposes it.

This opposition can’t be settled and resolved with some absurd “rainbow philosophy” that pretends to include everybody. It can’t be dismissed or merged in a melting lump of happy-happy cosmic cheese.

Those pseudo-philosophers who speak about consciousness as if it were one all-embracing ocean, within which we are merely tiny and ineffectual drops of water, have already developed a convenient amnesia about the artist.

Down through time, in the face of every spiritual system devised by the priest-class, the artist has said no. Instead, he has built his own worlds. He has lived the life of imagination, immune to the latest and greatest “New Age.”

He has asserted his power.

This is the natural mantle worn by the person who invents, imagines, improvises, creates: power.

Power that is apart from the group.

The artist not only sees, with great clarity, the mindless brain-dead gatherings of Collectives; he not only sees how they are built; he not only sees how they import “the highest ideals” to flesh out their slave-programs and objectives; he not only rejects all this; he creates something entirely different.

He invents worlds of his own. Many worlds.

The artist proliferates. He doesn’t reduce.

The artist isn’t looking for the “one thing” that will unite us all under a banner of harmony. He knows all such harmonies wear out and are eventually co-opted to produce mass hypnosis.

The artist rebels. In rebelling, he reveals the uniqueness of the individual. He doesn’t pay lip service to this uniqueness. He demonstrates it.

The artist destroys the Matrix, over and over.

Whether in art, science, philosophy, healing, or any other field of human endeavor, the person who lives by and through imagination creates new realities. As the artist, he challenges the status quo on every level.

This isn’t a superficial undertaking. It isn’t an attempt to “do something pretty and nice.” It isn’t part of “being a good citizen.”

The Collective is a fungus that seeks to swallow up people and nations. It enlists the highest-flying ideals as a cover. It sweeps away resistance with what seems like the most honorable of intentions.

Humanity on this planet has been undergoing a transformation into one ten-billion-member cult. You can find its leaders just by listening to their voices and their sentiments. They all come from the same manual.

This is really war by other means.

In the dying days of the engorged Roman Empire, which had squandered its capital through wars of conquest, it was decided that these other means were necessary. And so the Roman Church was invented. It would employ all the idealisms of past ages.

It would actually produce an unprecedented version of mind control as the weapon of conquest.

And today, we have “the Global outlook.” This is the silky cover for drawing in populations to a perverse dream of unity for all.

“We will harmonize the world.”

This is exactly the kind of program the artist has always rejected.

The artist says: there are an infinity of worlds, and they can exist side by side; artists create them.

When that message is lost, we lose what we are and enter into amnesia.

ROBOT OR FREE?

There are some people who hear the word CREATE and wake up, as if a new flashing music has begun.

This lone word makes them see something majestic and untamed and astonishing.

They feel the sound of a Niagara approaching.

They suddenly know why they are alive.

The creative life is about diving in. It’s about a kind of transformation that shreds programming and gets down to the energy of the Fire.

Most people don’t want to travel to that grand arena because they have been trained like pets by some sector of this society to be good girls and boys.

The creative life isn’t about little changes done in little penguin steps. It’s about putting your arms and your mind around Deep, Big, and Wide Desire. It’s about making that Desire come to life.

99% of the world has been trained like rats to adore systems. Give them a system and they’re ready to cuddle up and take it all in. If they have questions, or if they want to argue, it’s about how to tweak the system to make it a little better. And with every move they make, they put another blanket over the Fire Within.

They sleepwalk through life and say yes to everything.

Maybe you once saw something truly free that didn’t care about consequences, and it blew you into tomorrow and turned on your soul’s electricity for an hour.

Maybe you’re sick and tired of bowing and scraping before a pedestal of nonsense.

CREATE is a word that should be oceanic. It should shake and blow apart the pillars of the smug boredom of the soul.

CREATE is about what the individual does when he is on fire and doesn’t care about concealing it. It’s about what the individual invents when he has thrown off the false front that is slowly strangling him.

CREATE is about the end of mindless postponement. It’s about what happens when you burn up the pretty and petty little obsessions. It’s about emerging from the empty suit and empty machine of society that goes around and around and sucks away the vital bloodstream.

People want a certain level of defined comfort, and they want to BELONG TO SOMETHING.

“I want to belong. It’s my reason for being. It’s my hole card. Therefore, I’ll sit on my imagination, so it won’t take me out beyond this thing I want to attach myself to.”

The propaganda machines of society relentlessly turn out images and messages that ultimately say: YOU MUST BELONG TO THE GROUP.

Day after day after day, year after year, the media celebrate heroes. They inevitably interview these people to drag out of them the same old familiar stories. Have you EVER, even once, seen a hero who told an interviewer in no uncertain terms: “I got to where I am by denying the power of the group, by denying the propaganda that says we all have to BELONG.”

Have you ever heard that kind of uncompromising statement?

I didn’t think so.

Why not?

Because it’s not part of the BELONGING PROGRAM, the program that society runs on to stay away from the transforming power of IMAGINATION.

Jon Rappoport

The author of an explosive collection, THE MATRIX REVEALED, Jon was a candidate for a US Congressional seat in the 29th District of California. Nominated for a Pulitzer Prize, he has worked as an investigative reporter for 30 years, writing articles on politics, medicine, and health for CBS Health watch, LA Weekly, Spin Magazine, Stern, and other newspapers and magazines in the US and Europe. Jon has delivered lectures and seminars on global politics, health, logic, and creative power to audiences around the world. You can sign up for his free emails at www.nomorefakenews.com

Radio 3Fourteen - Jon Rappoport - The Artist Against the System

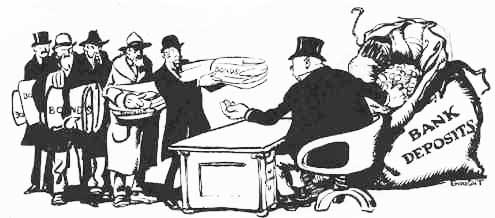

Other people's money, and how the bankers use it, 1914

CHAPTER 10 - THE INEFFICIENCY OF THE OLIGARCHS

Illustration from Harper's Weekly January 3, 1914 by Walter J. Enright

- By Justice Louis Brandeis -

We must break the Money Trust or the Money Trust will break us. The Interstate Commerce Commission said in its report on the most disastrous of the recent wrecks on the New Haven Railroad: "On this directorate were and are men whom the confiding public recognize as magicians in the art of finance, and wizards in the construction, operation, and consolidation of great systems of railroads. The public therefore rested secure that with the knowledge of the railroad art possessed by such men investments and travel should both be safe. Experience has shown that this reliance of the public was not justified as to either finance or safety." This failure of banker-management is not surprising. The surprise is that men should have supposed it would succeed. For banker-management contravenes the fundamental laws of human limitations: First, that no man can serve two masters; second, that a man cannot at the same time do many things well.

SEEMING SUCCESSES

There are numerous seeming exceptions to these rules; and a relatively few real ones. Of course, many banker-managed properties have been prosperous; some for a long time, at the expense of the public; some for a shorter time, because of the impetus attained before they were banker-managed. It is not difficult to have a large net income, where one has the field to oneself, has all the advantage privilege can give, and may "charge all the traffic will bear." And even in competitive business the success of a long-established, well-organized business with a widely extended good-will, must continue for a considerable time; especially if buttressed by intertwined relations constantly giving it the preference over competitors. The real test of efficiency comes when success has to be struggled for; when natural or legal conditions limit the charges which may be made for the goods sold or service rendered. Our banker-managed railroads have recently been subjected to such a test, and they have failed to pass it. "It is only,"' says Goethe, "when working within limitations, that the master is disclosed."

WHY OLIGARCHY FAILS

Banker-management fails, partly because the private interest destroys soundness of judgment and undermines loyalty. It fails partly, also, because banker directors are led by their occupation (and often even by the mere fact of their location remote from the operated properties) to apply a false test in making their decisions. Prominent in the banker-director mind is always this thought: "What will be the probable effect of our action upon the market value of the company's stock and bonds, or, indeed, generally upon stock exchange values?" The stock market is so much a part of the investment-banker's life, that he cannot help being affected by this consideration, however disinterested he may be. The stock market is sensitive. Facts are often misinterpreted "by the street'" or by investors. And with the best of intentions, directors susceptible to such influences are led to unwise decisions in the effort to prevent misinterpretations. Thus, expenditures necessary for maintenance, or for the ultimate good of a property are often deferred by banker-directors, because of the belief that the making of them now, would (by showing smaller net earnings), create a bad, and even false, impression on the market. Dividends are paid which should not be, because of the effect which it is believed reduction or suspension would have upon the market value of the company's securities. To exercise a sound judgment in the difficult affairs of business is, at best, a delicate operation. And no man can successfully perform that function whose mind is diverted, however innocently, from the study of, "what is best in the long run for the company of which I am director?" The banker-director is peculiarly liable to such distortion of judgment by reason of his occupation and his environment. But there is a further reason why, ordinarily, banker-management must fail.

THE ELEMENT OF TIME

The banker, with his multiplicity of interests, cannot ordinarily give the time essential to proper supervision and to acquiring that knowledge of the facts necessary to the exercise of sound judgment. The Century Dictionary tells us that a Director is "one who directs; one who guides, superintends, governs and manages." Real efficiency in any business in which conditions are ever changing must ultimately depend, in large measure, upon the correctness of the judgment exercised, almost from day to day, on the important problems as they arise. And how can the leading bankers, necessarily engrossed in the problems of their own vast private business, get time to know and to correlate the facts concerning so many other complex businesses? Besides, they start usually with ignorance of the particular business which they are supposed to direct. When the last paper was signed which created the Steel Trust, one of the lawyers (as Mr. Perkins frankly tells us) said: "That signature is the last one necessary to put the Steel industry, on a large scale, into the hands of men who do not know anything about it."

AVOCATIONS OF THE OLIGARCHS

The New Haven System is not a railroad, but an agglomeration of a railroad plus 121 separate corporations, control of which was acquired by the New Haven after that railroad attained its full growth of about 2,000 miles of line. In administering the railroad and each of the properties formerly managed through these 122 separate companies, there must arise from time to time difficult questions on which the directors should pass judgment. The real managing directors of the New Haven system during the decade of its decline were: J. Pierpont Morgan, George F. Baker, and William Rockefeller. Mr. Morgan was, until his death in 1913, the head of perhaps the largest banking house in the world. Mr. Baker was, until 1909, President and then Chairman of the Board of Directors of one of America's leading banks (the First National of New York), and Mr. Rockefeller was, until 1911, President of the Standard Oil Company. Each was well advanced in years. Yet each of these men, besides the duties of his own vast business, and important private interests, undertook to "guide, superintend, govern and manage," not only the New Haven but also the following other corporations, some of which were similarly complex: Mr. Morgan, 48 corporations, including 40 railroad corporations, with at least 100 subsidiary companies, and 16,000 miles of line; 3 banks and trust or insurance companies; 5 industrial and public service companies. Mr. Baker, 48 corporations, including 15 railroad corporations, with at least 158 subsidiaries; and 37,400 miles of track; 18 banks, and trust or insurance companies; 15 public-service corporations and industrial concerns. Mr. Rockefeller, 37 corporations, including 23 railroad corporations with at least 117 subsidiary companies, and 26,400 miles of line; 5 banks, trust or insurance companies; 9 public service companies and industrial concerns.

SUBSTITUTES

It has been urged that in view of the heavy burdens which the leaders of finance assume in directing Business-America, we should be patient of error and refrain from criticism, lest the leaders be deterred from continuing to perform this public service. A very respectable Boston daily said a few days after Commissioner McCord's report on the North Haven wreck: "It is believed that the New Haven pillory repeated with some frequency will make the part of railroad director quite undesirable and hard to fill, and more and more avoided by responsible men. Indeed it may even become so that men will have to be paid a substantial salary to compensate them in some degree for the risk involved in being on the board of directors." But there is no occasion for alarm. The American people have as little need of oligarchy in business as in politics. There are thousands of men in America who could have performed for the New Haven stockholders the task of one "who guides, superintends, governs and manages," better than did Mr. Morgan, Mr. Baker and Mr. Rockefeller. For though possessing less native ability, even the average business man would have done better than they, because working under proper conditions. There is great strength in serving with singleness of purpose one master only. There is great strength in having time to give to a business the attention which its difficult problems demand. And tens of thousands more Americans could be rendered competent to guide our important businesses. Liberty is the greatest developer. Herodotus tells us that while the tyrants ruled, the Athenians were no better fighters than their neighbors; but when freed, they immediately surpassed all others. If industrial democracy—true coöperation—should be substituted for industrial absolutism, there would be no lack of industrial leaders.

ENGLAND'S BIG BUSINESS

England, too, has big business. But her big business is the Coöperative Wholesale Society, with a wonderful story of 50 years of beneficent growth. Its annual turnover is now about $150,000,000—an amount exceeded by the sales of only a few American industrials; an amount larger than the gross receipts of any American railroad, except the Pennsylvania and the New York Central systems. Its business is very diversified, for its purpose is to supply the needs of its members. It includes that of wholesale dealer, of manufacturer, of grower, of miner, of banker, of insurer and of carrier. It operates the biggest flour mills and the biggest shoe factory in all Great Britain. It manufactures woolen cloths, all kinds of men's, women's and children's clothing, a dozen kinds of prepared foods, and as many household articles. It operates creameries. It carries on every branch of the printing business. It is now buying coal lands. It has a bacon factory in Denmark, and a tallow and oil factory in Australia. It grows tea in Ceylon. And through all the purchasing done by the Society runs this general principle: Go direct to the source of production, whether at home or abroad, so as to save commissions of middlemen and agents. Accordingly, it has buyers and warehouses in the United States, Canada, Australia, Spain, Denmark and Sweden. It owns steamers plying between Continental and English ports. It has an important banking department; it insures the property and person of its members. Every one of these departments is conducted in competition with the most efficient concerns in their respective lines in Great Britain. The Coöperative Wholesale Society makes its purchases, and manufactures its products, in order to supply the 1399 local distributive, coöperative societies scattered over all England; but each local society is at liberty to buy from the wholesale society, or not, as it chooses; and they buy only if the Coöperative Wholesale sells at market prices. This the Coöperative actually does; and it is able besides to return to the local a fair dividend on its purchases.

INDUSTRIAL DEMOCRACY

Now, how are the directors of this great business chosen? Not by England's leading bankers, or other notabilities, supposed to possess unusual wisdom; but democratically, by all of the people interested in the operations of the Society. And the number of such persons who have directly or indirectly a voice in the selection of the directors of the English Coöperative Wholesale Society is 2,750,000. For the directors of the Wholesale Society are elected by vote of the delegates of the 1399 retail societies. And the delegates of the retail societies are, in turn, selected by the members of the local societies;—that is, by the consumers, on the principle of one man, one vote, regardless of the amount of capital contributed. Note what kind of men these industrial democrats select to exercise executive control of their vast organization. Not all-wise bankers or their dummies, but men who have risen from the ranks of coöperation; men who, by conspicuous service in the local societies have won the respect and confidence of their fellows. The directors are elected for one year only; but a director is rarely un-seated. J. T. W. Mitchell was president of the Society continuously for 21 years. Thirty-two directors are selected in this manner. Each gives to the business of the Society his whole time and attention; and the aggregate salaries of the thirty-two is less than that of many a single executive in American corporations; for these directors of England's big business serve each for a salary of about $1500 a year. The Coöperative Wholesale Society of England is the oldest and largest of these institutions. But similar wholesale societies exist in 15 other countries. The Scotch Society (which William Maxwell has served most efficiently as President for thirty years at a salary never exceeding $38 a week) has a turn-over of more than $50,000,000 a year.

A REMEDY FOR TRUSTS

Albert Sonnichsen, General Secretary of the Cooperative League, tells in the American Review of Reviews for April, 1913, how the Swedish Wholesale Society curbed the Sugar Trust; how it crushed the Margerine Combine (compelling it to dissolve after having lost 2,300,000 crowns in the struggle); and how in Switzerland the Wholesale Society forced the dissolution of the Shoe Manufacturers Association. He tells also this memorable incident: "Six years ago, at an international congress in Cremona, Dr. Hans Müller, a Swiss delegate, presented a resolution by which an international wholesale society should be created. Luigi Luzzatti, Italian Minister of State and an ardent member of the movement, was in the chair. Those who were present say Luzzatti paused, his eyes lighted up, then, dramatically raising his hand, he said: ‘Dr. Muller proposes to the assembly a great idea—that of opposing to the great trusts, the Rockefellers of the world, a world-wide cooperative alliance which shall become so powerful as to crush the trusts.’ "

COOPERATION IN AMERICA

America has no Wholesale Cooperative Society able to grapple with the trusts. But it has some very strong retail societies, like the Tamarack of Michigan, which has distributed in dividends to its members $1,144,000 in 23 years. The recent high cost of living has greatly stimulated interest in the cooperative movement; and John Graham Brooks reports that we have already about 350 local distributive societies. The movement toward federation is progressing. There are over 100 cooperative stores in Minnesota, Wisconsin and other Northwestern states, many of which were organized by or through the zealous work of Mr. Tousley and his associates of the Right Relationship League and are in some ways affiliated. In New York City 83 organizations are affiliated with the Cooperative League. In New Jersey the societies have federated into the American Cooperative Alliance of Northern New Jersey. In California, long the seat of effective cooperative work, a central management committee is developing. And progressive Wisconsin has recently legislated wisely to develop cooperation throughout the state. Among our farmers the interest in cooperation is especially keen. The federal government has just established a separate bureau of the Department of Agriculture to aid in the study, development and introduction of the best methods of cooperation in the working of farms, in buying, and in distribution; and special attention is now being given to farm credits—a field of cooperation in which Continental Europe has achieved complete success, and to which David Lubin, America's delegate to the International Institute of Agriculture at Rome, has, among others, done much to direct our attention.

PEOPLE'S SAVINGS BANKS

The German farmer has achieved democratic banking. The 13,000 little cooperative credit associations, with an average membership of about 90 persons, are truly banks of the people, by the people and for the people. First: The banks' resources are of the people. These aggregate about $500,000,000. Of this amount $375,000,000 represents the farmers' savings deposits; $50,000,000, the farmers' current deposits; $6,000,000, the farmers' share capital; and $13,000,000, amounts earned and placed in the reserve. Thus, nearly nine-tenths of these large resources belong to the farmers—that is, to the members of the banks. Second: The banks are managed by the people—that is, the members. And membership is easily attained; for the average amount of paid-up share capital was, in 1909, less than $5 per member. Each member has one vote regardless of the number of his shares or the amount of his deposits. These members elect the officers. The committees and trustees (and often even, the treasurer) serve without pay: so that the expenses of the banks are, on the average, about $150 a year. Third: The banks are for the people. The farmers' money is loaned by the farmer to the farmer at a low rate of interest (usually 4 per cent. to 6 per cent.); the shareholders receiving, on their shares, the same rate of interest that the borrowers pay on their loans. Thus the resources of all farmers are made available to each farmer, for productive purposes. This democratic rural banking is not confined to Germany. As Henry W. Wolff says in his book on cooperative banks: "Propagating themselves by their own merits, little people's cooperative banks have overspread Germany, Italy, Austria, Hungary, Switzerland, Belgium. Russia is following up those countries; France is striving strenuously for the possession of cooperative credit. Servia, Roumania, and Bulgaria have made such credit their own. Canada has scored its first success on the road to its acquisition. Cyprus, and even Jamaica, have made their first start. Ireland has substantial first-fruits to show of her economic sowings. "South Africa is groping its way to the same goal. Egypt has discovered the necessity of cooperative banks, even by the side of Lord Cromer's pet creation, the richly endowed `agricultural bank.' India has made a beginning full of promise. And even in far Japan, and in China, people are trying to acclimatize the more perfected organizations of Schulze-Delitzsch and Raffeisen. The entire world seems girdled with a ring of cooperative credit. Only the United States and Great Britain still lag lamentably behind."

BANKERS' SAVINGS BANKS

The savings banks of America present a striking contrast to these democratic banks. Our savings banks also have performed a great service. They have provided for the people's funds safe depositories with some income return. Thereby they have encouraged thrift and have created, among other things, reserves for the proverbial "rainy day." They have also discouraged "old stocking" hoarding, which diverts the money of the country from the channels of trade. American savings banks are also, in a sense, banks of the people; for it is the people's money which is administered by them. The $4,500,000,000 deposits in 2,000 American savings banks belong to about ten million people, who have an average deposit of about $450. But our savings banks are not banks by the people, nor, in the full sense, for the people. First: American savings banks are not managed by the people. The stock-savings banks, most prevalent in the Middle West and the South, are purely commercial enterprises, managed, of course, by the stockholders’ representatives. The mutual savings banks, most prevalent in the Eastern states, have no stockholders; but the depositors have no voice in the management. The banks are managed by trustees for the people, practically a self-constituted and self-perpetuating body, composed of "leading" and, to a large extent, public-spirited citizens. Among them (at least in the larger cities) there is apt to be a predominance of investment bankers, and bank directors. Thus the three largest savings banks of Boston (whose aggregate deposits exceed those of the other 18 banks) have together 81 trustees. Of these, 52 are investment bankers or directors in other Massachusetts banks or trust companies. Second: The funds of our savings banks (whether stock or purely mutual) are not used mainly for the people. The depositors are allowed interest (usually from 3 to 4 per cent.). In the mutual savings banks they receive ultimately all the net earnings. But the money gathered in these reservoirs is not used to aid productively persons of the classes who make the deposits.

The depositors are largely wage earners, salaried people, or members of small tradesmen's families. Statically the money is used for them. Dynamically it is used for the capitalist. For rare, indeed, are the instances when savings banks' moneys are loaned to advance productively one of the depositor class. Such persons would seldom be able to provide the required security; and it is doubtful whether their small needs would, in any event, receive consideration. In 1912 the largest of Boston's mutual savings banks—the Provident Institution for Savings, which is the pioneer mutual savings bank of America—managed $53,000,000 of people’s money. Nearly one-half of the resources ($24,262,072) was invested in bonds—state, municipal, railroad, railway and telephone and in bank stock; or was deposited in national banks or trust companies. Two-fifths of the resources ($20,764,770) were loaned on real estate mortgages; and the average amount of a loan was $52,569. One-seventh of the resources ($7,566,612) was loaned on personal security; and the average of each of these loans was $54,830. Obviously, the "small man" is not conspicuous among the borrowers; and these large-scale investments do not even serve the individual depositor especially well; for this bank pays its depositors a rate of interest lower than the average. Even our admirable Postal Savings Bank system serves productively mainly the capitalist. These postal saving stations are in effect catch-basins merely, which collect the people's money for distribution among the national banks.

PROGRESS

Alphonse Desjardins of Levis, Province of Quebec, has demonstrated that cooperative credit associations are applicable, also, to at least some urban communities. Levis, situated on the St. Lawrence opposite the City of Quebec, is a city of 8,000 inhabitants. Desjardins himself is a man of the people. Many years ago he became impressed with the fact that the people's savings were not utilized primarily to aid the people productively. There were then located in Levis branches of three ordinary banks of deposit—a mutual savings bank, the postal savings bank, and three incorporated "loaners"; but the people were not served. After much thinking, he chanced to read of the European rural banks. He proceeded to work out the idea for use in Levis; and in 1900 established there the first "credit-union." For seven years he watched carefully the operations of this little bank. The pioneer union had accumulated in that period $80,000 in resources. It had made 2,900 loans to its members, aggregating $350,000; the loans averaging $120 in amount, and the interest rate 6 1/2 per cent. In all this time the bank had not met with a single loss. Then Desjardins concluded that democratic banking was applicable to Canada; and he proceeded to establish other credit-unions. In the last 5 years the number of credit-unions in the Province of Quebec has grown to 121; and 19 have been established in the Province of Ontario. Desjardins was not merely the pioneer. All the later credit-unions also have been established through his aid; and 24 applications are now in hand requesting like assistance from him. Year after year that aid has been given without pay by this public-spirited man of large family and small means, who lives as simply as the ordinary mechanic. And it is noteworthy that this rapidly extending system of cooperative credit-banks has been established in Canada wholely without government aid, Desjardins having given his services free, and his travelling expenses having been paid by those seeking his assistance.

In 1909, Massachusetts, under Desjardins' guidance, enacted a law for the incorporation of credit-unions. The first union established in Springfield, in 1910, was named after Herbert Myrick—a strong advocate of cooperative finance. Since then 25 other unions have been formed; and the names of the unions and of their officers disclose that 11 are Jewish, 8 French-Canadian, and 2 Italian—a strong indication that the immigrant is not unprepared for financial democracy. There is reason to believe that these people's banks will spread rapidly in the United States and that they will succeed. For the cooperative building and loan associations, managed by wage-earners and salary-earners, who joined together for systematic saving and ownership of houses—have prospered in many states. In Massachusetts, where they have existed for 35 years, their success has been notable—the number, in 1912, being 162, and their aggregate assets nearly $75,000,000.

Thus farmers, workingmen, and clerks are learning to use their little capital and their savings to help one another instead of turning over their money to the great bankers for safe keeping, and to be themselves exploited. And may we not expect that when the cooperative movement develops in America, merchants and manufacturers will learn from farmers and workingmen how to help themselves by helping one another, and thus join in attaining the New Freedom for all? When merchants and manufacturers learn this lesson, money kings will lose subjects, and swollen fortunes may shrink; but industries will flourish, because the faculties of men will be liberated and developed.

President Wilson has said wisely:

"No country can afford to have its prosperity originated by a small controlling class. The treasury of America does not lie in the brains of the small body of men now in control of the great enterprises… It depends upon the inventions of unknown men, upon the originations of unknown men, upon the ambitions of unknown men. Every country is renewed out of the ranks of the unknown, not out of the ranks of the already famous and powerful in control."

Return to the table of contents

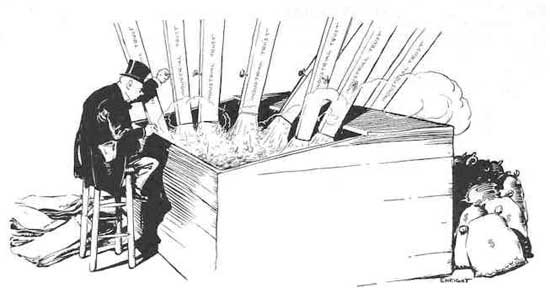

Other people's money, and how the bankers use it, 1914

CHAPTER 9 - THE FAILURE OF BANKER-MANAGEMENT

Illustration from Harper's Weekly December 27, 1913 by Walter J. Enright

- By Justice Louis Brandeis -

There is not one moral, but many, to be drawn from the Decline of the New Haven and the Fall of Mellen. That history offers texts for many sermons. It illustrates the Evils of Monopoly, the Curse of Bigness, the Futility of Lying, and the Pitfalls of Law-Breaking. But perhaps the most impressive lesson that it should teach to investors is the failure of banker-management.

BANKER CONTROL

For years J. P. Morgan & Co. were the fiscal agents of the New Haven. For years Mr. Morgan was the director of the Company. He gave to that property probably closer personal attention than to any other of his many interests. Stockholders' meetings are rarely interesting or important; and few indeed must have been the occasions when Mr. Morgan attended any stockholders' meeting of other companies in which he was a director. But it was his habit, when in America, to be present at meetings of the New Haven. In 1907, when the policy of monopolistic expansion was first challenged, and again at the meeting in 1909 (after Massachusetts had unwisely accorded its sanction to the Boston & Maine merger), Mr. Morgan himself moved the large increases of stock which were unanimously voted. Of course, he attended the important directors' meeting. His will was law. President Mellen indicated this in his statement before Interstate Commerce Commissioner Prouty, while discussing the New York, Westchester & Boston—the railroad without a terminal in New York, which cost the New Haven $1,500,000 a mile to acquire, and was then costing it, in operating deficits and interest charges, $100,000 a month to run:

"I am in a very embarrassing position, Mr. Commissioner, regarding the New York, Westchester & Boston. I have never been enthusiastic or at all optimistic of its being a good investment for our company in the present, or in the immediate future; but people in whom I had greater confidence than I have in myself thought it was wise and desirable; I yielded my judgment; indeed, I don't know that it would have made much difference whether I yielded or not."

THE BANKER'S RESPONSIBILITY

Bankers are credited with being a conservative force in the community. The tradition lingers that they are preeminently "safe and sane." And yet, the most grievous fault of this banker-managed railroad has been its financial recklessness—a fault that has already brought heavy losses to many thousands of small investors throughout New England for whom bankers are supposed to be natural guardians. In a community where its railroad stocks have for generations been deemed absolutely safe investments, the passing of the New Haven and of the Boston & Maine dividends after an unbroken dividend record of generations comes as a disaster.

This disaster is due mainly to enterprises outside the legitimate operation of these railroads; for no railroad company has equaled the New Haven in the quantity and extravagance of its outside enterprises. But it must be remembered, that neither the president of the New Haven nor any other railroad manager could engage in such transactions without the sanction of the Board of Directors. It is the directors, not Mr. Mellen, who should bear the responsibility.

Close scrutiny of the transactions discloses no justification. On the contrary, scrutiny serves only to make more clear the gravity of the errors committed. Not merely were recklessly extravagant acquisitions made in mad pursuit of monopoly; but the financial judgment, the financiering itself, was conspicuously bad. To pay for property several times what it is worth, to engage in grossly unwise enterprises, are errors of which no conservative directors should be found guilty; for perhaps the most important function of directors is to test the conclusions and curb by calm counsel the excessive zeal of too ambitious managers. But while we have no right to expect from bankers exceptionally good judgment in ordinary business matters; we do have a right to expect from them prudence, reasonably good financiering, and insistence upon straightforward accounting. And it is just the lack of these qualities in the New Haven management to which the severe criticism of the Interstate Commerce Commission is particularly directed.

Commissioner Prouty calls attention to the vast increase of capitalization. During the nine years beginning July 1, 1903, the capital of the New York, New Haven & Hartford Railroad Company itself increased from $93,000,000 to about $417,000,000 (excluding premiums). That fact alone would not convict the management of reckless financiering ; but the fact that so little of the new capital was represented by stock might well raise a question as to its conservativeness. For the indebtedness (including guaranties) was increased over twenty times (from about $14,000,000 to $300,000,000), while the stock outstanding in the hands of the public was not doubled ($80,000,000 to $158,000,000). Still, in these days of large things, even such growth of corporate liabilities might be consistent with "safe and sane management."

But what can be said in defense of the financial judgment of the banker-management under which these two railroads find themselves confronted, in the fateful year 1913, with a most disquieting floating indebtedness? On March 31, the New Haven had outstanding $43,000,000 in short-time notes; the Boston & Maine had then outstanding $24,500,000, which have been increased since to $27,000,000; and additional notes have been issued by several of its subsidiary lines. Mainly to meet its share of these loans, the New Haven, which before its great expansion could sell at par 3 1/2 per cent. bonds convertible into stock at $150 a share, was so eager to issue at par $67,500,000 of its 6 per cent. 20-year bonds convertible into stock as to agree to pay J. P. Morgan & Co. a 2 1/2 per cent. underwriting commission. True, money was "tight" then. But is it not very bad financiering to be so unprepared for the "tight" money market which had been long expected? Indeed, the New Haven's management, particularly, ought to have avoided such an error; for it committed a similar one in the "tight" money market of 1907-1908, when it had to sell at par $39,000,000 of its 6 per cent. 40-year bonds.

These huge short-time borrowings of the System were not due to unexpected emergencies or to their monetary conditions. They were of gradual growth. On June 30, 1910, the two companies owed in short-term notes only $10,180,364; by June 30, 1911, the amount had grown to $30,759,959; by June 30, 1912, to $45,395,000; and in 1913 to over $70,000,000. Of course the rate of interest on the loans increased also very largely. And these loans were incurred unnecessarily. They represent, in the main, not improvements on the New Haven or on the Boston & Maine Railroads, but money borrowed either to pay for stocks in other companies which these companies could not afford to buy, or to pay dividends which had not been earned.

In five years out of the last six the New Haven Railroad has, on its own showing, paid dividends in excess of the year's earnings; and the annual deficits disclosed would have been much larger if proper charges for depreciation of equipment and of steamships had been made. In each of the last three years, during which the New Haven had absolute control of the Boston & Maine, the latter paid out in dividends so much in excess of earnings that before April, 1913, the surplus accumulated in earlier years had been converted into a deficit.

Surely these facts show, at least, an extraordinary lack of financial prudence.

WHY BANKER-MANAGEMENT FAILED

Now, how can the failure of the banker-management of the New Haven be explained?

A few have questioned the ability; a few the integrity of the bankers. Commissioner Prouty attributed the mistakes made to the Company's pursuit of a transportation monopoly.

"The reason," says he, "is as apparent as the fact itself. The present management of that Company started out with the purpose of controlling the transportation facilities of New England. In the accomplishment of that purpose it bought what must be had and paid what must be paid. To this purpose and its attempted execution can be traced every one of these financial misfortunes and derelictions."

But it still remains to find the cause of the bad judgment exercised by the eminent banker-management in entering upon and in carrying out the policy of monopoly. For there were as grave errors in the execution of the policy of monopoly as in its adoption. Indeed, it was the aggregation of important errors of detail which compelled first the reduction, then the passing of dividends and which ultimately impaired the Company's credit.

The failure of the banker-management of the New Haven cannot be explained as the shortcomings of individuals. The failure was not accidental. It was not exceptional. It was the natural result of confusing the functions of banker and business man.

UNDIVIDED LOYALTY

The banker should be detached from the business for which he performs the banking service. This detachment is desirable, in the first place, in order to avoid conflict of interest. The relation of banker-directors to corporations which they finance has been a subject of just criticism. Their conflicting interests necessarily prevent single-minded devotion to the corporation. When a banker-director of a railroad decides as railroad man that it shall issue securities, and then sells them to himself as banker, fixing the price at which they are to be taken, there is necessarily grave danger that the interests of the railroad may suffer—suffer both through issuing of securities which ought not to be issued, and from selling them at a price less favorable to the company than should have been obtained. For it is ordinarily impossible for a banker-director to judge impartially between the corporation and himself. Even if he succeeded in being impartial, the relation would not conduce to the best interests of the company. The best bargains are made when buyer and seller are represented by different persons.

DETACHMENT AN ESSENTIAL

But the objection to banker-management does not rest wholly, or perhaps mainly, upon the importance of avoiding divided loyalty. A complete detachment of the banker from the corporation is necessary in order to secure for the railroad the benefit of the clearest financial judgment; for the banker's judgment will be necessarily clouded by participation in the management or by ultimate responsibility for the policy actually pursued. It is outside financial advice which the railroad needs.

Long ago it was recognized that "a man who is his own lawyer has a fool for a client." The essential reason for this is that soundness of judgment is easily obscured by self-interest. Similarly, it is not the proper function of the banker to construct, purchase, or operate railroads, or to engage in industrial enterprises. The proper function of the banker is to give to or to withhold credit from other concerns; to purchase or to refuse to purchase securities from other concerns; and to sell securities to other customers. The proper exercise of this function demands that the banker should be wholly detached from the concern whose credit or securities are under consideration. His decision to grant or to withhold credit, to purchase or not to purchase securities, involves passing judgment on the efficiency of the management or the soundness of the enterprise; and he ought not to occupy a position where in so doing he is passing judgment on himself. Of course detachment does not imply lack of knowledge. The banker should act only with full knowledge, just as a lawyer should act only with full knowledge. The banker who undertakes to make loans to or purchase securities from a railroad for sale to his other customers ought to have as full knowledge of its affairs as does its legal adviser. But the banker should not be, in any sense, his own client. He should not, in the capacity of banker, pass judgment upon the wisdom of his own plans or acts as railroad man.

Such a detached attitude on the part of the banker is demanded also in the interest of his other customers—the purchasers of corporate securities. The investment banker stands toward a large part of his customers in a position of trust, which should be fully recognized. The small investors, particularly the women, who are holding an ever-increasing proportion of our corporate securities, commonly buy on the recommendation of their bankers. The small investors do not, and in most cases cannot, ascertain for themselves the facts on which to base a proper judgment as to the soundness of securities offered. And even if these investors were furnished with the facts, they lack the business experience essential to forming a proper judgment. Such investors need and are entitled to have the bankers' advice, and obviously their unbiased advice; and the advice cannot be unbiased where the banker, as part of the corporation's management, has participated in the creation of the securities which are the subject of sale to the investor.

Is it conceivable that the great house of Morgan would have aided in providing the New Haven with the hundreds of millions so unwisely expended, if its judgment had not been clouded by participation in the New Haven's management?

Go to the next chapter

Return to the table of contents

- You are here:

-

Home

- Articles