Dissent Into Madness - Political Psychopathy - Must Watch

What if the delusions of the dissidents are in fact real? What if their paranoid fantasies are not fantasies at all? In other words, what if it is not the political dissidents who are crazy, but the politicians?

You are about to learn the dark history and the even more disturbing present of political psychopathy, “mental illness and disorder”. Made possible by “Diagnostic and Statistical Manual of Mental Disorders (DSM)”

Ballot Initiative, Or Citizens Referendum Enterprise

Published: March 13, 2025 - By We, The American People

In recent years, the psychopath parasite ruling cabal (PRC) and their prostituted politicians focused on their own special interest and agendas, have been subverting the will of we, the American people, by refusing to implement United States Constitution and voter-approved, or voters demanded initiatives, thus continue introducing and implementing nefarious bills, laws tightening the PRC’s shackles, thus making it impossible for we, the people to propose and pass new ethical, patriotic, humane and user friendly laws by means of Ballot Initiative, Or Citizens Referendum.

We, the American people, must never forget the vital fact that United States Constitution is the absolute supreme law of the land. United States Constitution supersedes ALL states and federal laws. Thereby ALL unconstitutional statutes, each and every conflicting laws are null and void.

We, the American people, must nullify the said unconstitutional edicts. We, the people, are at the top, final decision makers. We, the people, must put in place laws, which will protect our rights, lives, family, country and property.

Ballot Initiative allows we, the American people, to propose, vote and approve laws and or constitutional amendments necessary to protect and defend United States, American people and our democracy. We must understand that PRC’s Money and financial influences on our government are not speech, thereby we must elect and establish a government, free from toxic influences, focused on America first only.

Usury is the illegal action, or practice of lending money at unreasonably high rates of interest. Take a wild guess whom are involved making trillions of dollars forcing “USURY” on people allover planet Earth?

Utilizing Ballot Initiative, Citizens Referendum Americanism Measures Across The United States is the only peaceful means of returning the control of our country, our lives, our families and our state and national governments to We, The American People.

1 - Abolishing, Terminating The Unconstitutional, And Treasonous 1913 Federal Reserve Act And The Income Tax Law - To prevent United States devastating depression and economic collapse, We, The American People, hereby nullify, repeal, and terminate the 1913 Federal Reserve Act and Income Tax Law. - Prior to the said treasonous act United States money supply used to be printed as “CREDIT”, which deliberately was replaced with money printed as “DEBT”. - We, The American People, hereby nationalize the Federal Reserve, and all of its subsidiaries, companies, branches, properties, securities, stocks, bonds and precious metals, plus all resources and deposits, known and unknown, in perpetuity, thereby wiping-out the United States unconstitutional, fraudulent and illegal $37 TRILLION debt obligation and interest for good. - The owners of Federal Reserve have already embezzled and pocketed far more than $37 TRILLION since the inception of the 1913 Unconstitutional, and Treasonous Federal Reserve Act.

2 - Local and National Election Constitutional Amendment - We, the American people, must nullify Mail-in and Absentee Ballots, plus all Electronic voting systems and procedures, thereby replacing them with Paper Ballots, in person voting only. We must mandate paper ballot and in person voting election as the only means of conducting all local, state and national elections. We, the American people, must also lower the voting age to 17 years, requiring valid U.S. Citizen voter identification to be presented at the ballot box.

3 - Public Property Preservation Law, In Opposition Of Rent Slavery - We, the American people, must always be wary of “MONOPOLY”, the deliberate exclusive possession of numerous farmlands, residential homes, apartments, and property, thereby causing price hike and scarcity, which will lead to excluding We, the American people, the chance of ownership of our own home, farm, apartment, property, thus remain “RENT SLAVES”. Thereby creating unfair, greedy price hikes and control, for the sole benefit and dominance of the psychopath parasite ruling cabal (PRC). The control of supply of any commodity, or service by the PRC is for their own monopolistic greedy benefits only. Thereby We, the American people, mandate the “PUBLIC PROPERTY PRESERVATION LAW”, prohibiting states and federal governments, foreign, and or domestic corporate ownership of farmlands and residential homes, apartments and any other forms of agricultural and residential properties. All of the said properties must be sold off to the tenants occupying the said properties, or the unoccupied properties must be offered to first time farm, or home buying individual American buyers at the purchasing price, or lower, depending on the circumstances of each property at the time of original perches. The individual American buyers are allowed to purchase a farm and a home for personal use, benefiting them and their family. Therefore no one is allowed to purchase multiple (more than one) property for investment purposes.

4 - Equal Representation Of Male And Female Citizens - We, the American people, mandating a national law, making it compulsory to elect equal number of true biological female and male (1 woman and 1 man) from every municipality of every state in the union, to represent all of We, the American people, at local and national legislative bodies. Thus presenting women and men equal voice, equal rights and equal vote, to build and maintain a true responsive, prosperous, just and impartial social governing system for all Americans.

5 - Term Limiting Members Of Congress - We, the American people, hereby mandating a national law, authorizing National and State senators to serve maximum of six (6) years in office. Also authorizing States assembly and House of Representatives members to serve maximum of four (4) years in office. The elected Representatives (local and or national) while in office are not allowed to run for any other office. If any Representatives chooses to run for another political office, they must permanently resign their current elected position beforehand.

6 - Patriotic Devotion, Political Integrity And Honor - Hereby We, The American People, enact a national law, compelling all appointed, selected and or elected officials and politicians to behave in dignified and honest manner. Thereby reminding all of us that breaking the oath of office and turning against we, the American people, is treason, punishable by law. Receiving any pay-offs, kickbacks, gifts, and or bribes, euphemistically called: “Campaign Contributions" are all treasonous acts. Both the corruptie (bribe giver) and the corrupted (bribe receiver) shall be indicted and locked up for crime of treason, racketeering and grand larceny.

7 - Limiting Presidential Pardon Powers - We, the American people, must prevent the criminal parasite ruling class to commit treasonous acts, while relying on presidential pardons to be forgiven at the end of the said presidential term. Thereby Presidential Pardons must be issued by the president him / herself, for none treasonous acts only. Thus each president will be held accountable by law, for issuing invalid and unlawful pardons.

8 - The Parasite Ruling Class And Their Shadowy Government Cessation - We, the American people, hereby enact treason national law, prohibiting, and preventing all judges, courts, government agencies and officials, politicians, plus all local and national legislative bodies from amending, suspending, removing, or misinterpreting any and all rules and regulations enacted by; WE, THE AMERICAN PEOPLE, through national and or local ballot initiatives, referendums. Hereby the order of We, the American people, all “Qualified Immunity” of all local and national government employees and politicians are null and void, and could never be reinstated. From this point forth TRUTH & TRANSPARENCY shall be the one and only way to conduct all our social, economic, political and government affairs.

9 - One-Time Nationwide Blanket Pardon - We, the American people, hereby mandate a one-time pardon for our servant politicians, government employees and the private sector working for the so called shadowy government, or invisible enemy, or deep state, or the Parasite Ruling Class, or "Obvious State". This one time AMNESTY is to provide the opportunity for those who wish to return HOME, back into the open arms of the American people, to repent and begin anew. Hereby all secrets, top secrets and generally all classified documents of any kind are declassified, and must be displayed on each of the related government agency websites, in their entirety without any redactions.

10 - Power Corrupts, Absolute Power Corrupts Absolutely - We, the American people, mandate that all STATES and the FEDERAL GOVERNMENT must balance their budget each year. We, the American people, are the one and only source of authority to make and approve ALL decisions regarding all WARS, HEALTH MATTERS, DEMOCRACY, All TAXES, STATE AND FEDERAL BUDGET, MONEY, ELECTIONS, ENVIRONMENT, JUDICIAL SYSTEM, EMIGRATION, plus ARTIFICIAL INTELLIGENCE (AI) Policies, Rules and Regulations, in addition to all other currently unknown, including future related issues. - Thereby all described laws, rules and directives must be decided by We, the American people, through sixty-five percent (65%) majority approved Ballot Initiative, Or Citizens Referendum, exclusively by We, the American people.

United We Prosper, Divided We Die.

"We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable rights, that among these are life, liberty and the pursuit of happiness. That to secure these rights, governments are instituted among men, deriving their just powers from the consent of the governed. That whenever any form of government becomes destructive to these ends, it is the right of the people to alter or to abolish it, and to institute new government, laying its foundation on such principles and organizing its powers in such form, as to them shall seem most likely to effect their safety and happiness." - United States of America - Declaration of Independence, July 04, 1776.

Eugenics - An Evil, Immoral And Pseudoscientific Ideology

- By Bahram Maskanian - March 09, 2017

The parasite ruling class psychopaths has always been searching for viable false flag operation to be used for castrating, sterilizing countless men and women. And or murder large number of innocent children, women and men under the umbrella of protecting the nation, by waging wars, committing genocide, or using public health and safety excuses to reduce population for tighter and easier control.

Eugenics was coined the science of improving human population by controlled breeding to increase the occurrence of desirable heritable characteristics. Developed largely by Charles Darwin and his cousin Francis Galton in Britain starting in 1883. The so called method of improving the human race, fell into disfavor only after the Nazi Germany overtly begin using Eugenics doctrines.

Eugenics Society of America was founded by Andrew Carnegie in the United States. America's first general-purpose philanthropic foundations: Russell Sage (founded 1907), Carnegie (1911), and Rockefeller (1913) they all funded and backed eugenics, precisely encouraging the efforts to promote the reproduction of the “fit” and to suppress the reproduction of the “unfit”.

The nefarious parasite ruling class Eugenics Ideology, rejects Natural Law, that all human beings are created equal, thus redefine humanity purely in terms of mythical genetic superiority. Eugenics racist doctrine includes pursuit of pure genetic pool, and elimination of the ”Unfit Races”, or 95% of humanity on planet Earth.!

Eugenics (population reduction) has many different branches one of which is “Transhumanism” a new way of thinking about the humanity’s future, based on the premise that the human species in its current form is too dumb and not good enough to live in today’s world of high tech. Therefore robotic elements must be incorporated into humans to increase the survival chance of humanity based on the eugenics vision and ideology.

The obvious truth we, the people are not told is the fact that all universities, governments and human rights organizations are completely aware that the best population reduction is health, happiness and prosperity. Healthy, Happy and prosperous people all over the world will have less children in time of peace and prospers environment. Therefore if anyone still advocating Eugenics should stop, investigate, read and think.

We, the people must be mindful of all propaganda reported. The mass media by not reporting the truth legitimizes mass murder of war. In fact, mass medias talking heads and operators are the real terrorist for deliberately covering up the truth and hypnotizing the public to allow the government to conduct wars of aggression, thus achieving more of the parasite ruling class’s world domination, political and economic objectives by murdering millions of innocent children, women and men.

The same propaganda dissemination is also used regarding world’s population. Where the closeted ordinary Eugenist folks, secretly approve Eugenics operations based on their ignorance of the facts.

The U.S. Census Bureau who has army of paid foot soldiers to go door to door, failed year after year to accurately count America’s population, has setup a “World Population Clock” to guess the world population. - Again a computer model, concocted by the parasite ruling class, where the programmers can easily manipulate the outcome, thus broadcasting the needed estimate for Eugenics mass murder justification, that as of September 2022, world population will be - 7,922,312,800 - people and is expected to reach…! The fact is that world population has been declining since late 1970s to four billion by 2020.

Knowledge is power.! We, the people can easily initiate changes and reforms necessary by first and foremost educating ourselves, our loved ones and friends. To remedy humanity’s current tyrannical situation peacefully, using nonviolent resistance, we must share what we learn, that CIA, British intelligence and others like them work for the committee of 300 low-level crime families, whom are under the control of the symbolically alluded to as the thirteen top families; known as: “Deep State”, or “Ruling Oligarchy”, or “Parasite Ruling Class”, or “Secret Cabal”, or “Illamanaties”, or “Zionists”, or “Eugenist”, or “Nation-less Corporations”, or Multi Nationals, or “City of London”, etc., they are all referring to the same nefarious families secretly controlling planet Earth. The top of the pyramid families are as follows:

Mellons, Carnegies, Rothschilds, Rockefellers, Schiffs, Dukes, Astors, Dorrances, Reynoldses, Stilimans, Bakers, Pynes, Cuilmans, Watsons, Tukes, Kleinworts, DuPonts, Warburgs, Phippses, Graces, Guggenheims, Milners, Drexels, Winthrops, Vanderbilts, Whitneys, Harknesses, along with few other filthy rich billionaires, controlling everything. - - “Bloodlines of Illuminati” - By Fritz Springmeier

They are overtly poisoning our air, called geo-engineering, or chem-trails, spraying toxic chemicals into the atmosphere from aircrafts high above, while we are lied to and vaccinated with toxic chemicals, as our produce and foods are contaminated with highly toxic GMOs and chemical herbicides and fertilizers, and our water with fluoride. Marching towards their Eugenics goals. And these are what we know.!

Toxicology vs Virology - Rockefeller Institute and the Criminal Polio Fraud - By Dr. Sam Bailey

Read and or download a free copy, everybody must read this amazing factual book.

* Bloodlines of Illuminati - By Fritz Springmeier

* Alex Thomson - UK Column - Grand Jury Proceeding the Court of Public Opinion

* Interview 1766 - The Underpopulation Bomb - #NewWorldNextWeek

1984

- 1949 - By George Orwell - 393 Pages

George Orwell's dystopian masterpiece, Nineteen Eighty-Four is perhaps the most pervasively influential book of the twentieth century, making famous Big Brother, newspeak and Room 101.

'Who controls the past controls the future: who controls the present controls the past'

Hidden away in the Record Department of the sprawling Ministry of Truth, Winston Smith skilfully rewrites the past to suit the needs of the Party. Yet he inwardly rebels against the totalitarian world he lives in, which demands absolute obedience and controls him through the all-seeing telescreens and the watchful eye of Big Brother, symbolic head of the Party. In his longing for truth and liberty, Smith begins a secret love affair with a fellow-worker Julia, but soon discovers the true price of freedom is betrayal.

Download 1984

This book was published in Australia and is out of copyright. Be sure to check the copyright laws for your country before downloading, reading or sharing this PDF file.

Who financed Lenin and Trotsky's Bolshevik Revolution?

The Creature from Jekyll Island

- By G. Edward Griffin - Page 123:

The top Communist leaders have never been as hostile to their counterparts in the West, as the rhetoric suggests. They are quite friendly to the world's leading financiers and have worked closely with them, when it suits their purposes. As we shall see in the following section, the Bolshevik revolution actually was financed by wealthy financiers in London and New York. Lenin and Trotsky were on the closest of terms with these moneyed interests both before and after the Revolution. Those hidden liaisons have continued to this day and occasionally pop to the surface, when we discover a David Rockefeller holding confidential meetings with a Mikhail Gorbachev in the absence of government sponsorship or diplomatic purpose.

Pages 263-267:

Chapter 13 - MASQUERADE IN MOSCOW

One of the greatest myths of contemporary history is that the Bolshevik Revolution in Russia was a popular uprising of the downtrodden masses against the hated ruling class of the Tsars. As we shall see, however, the planning, the leadership and especially the financing came entirely from outside Russia, mostly from financiers in Germany, Britain and the United States. Furthermore we shall see, that the Rothschild Formula played a major role in shaping these events.

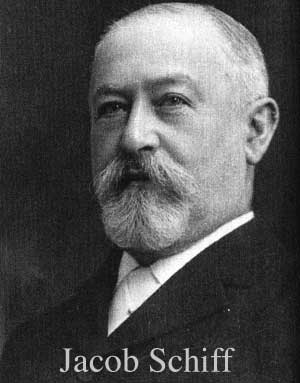

This amazing story begins with the war between Russia and Japan in 1904. Jacob Schiff, who was head of the New York investment firm Kuhn, Loeb and Company, had raised the capital for large war loans to Japan. It was due to this funding that the Japanese were able to launch a stunning attack against the Russians at Port Arthur and the following year to virtually decimate the Russian fleet. In 1905 the Mikado awarded Jacob Schiff a medal, the Second Order of the Treasure of Japan, in recognition of his important role in that campaign.

|

| Jacob Schiff was head of the New York investment firm Kuhn, Loeb and Co. He was one of the principal backers of the Bolshevik revolution and personally financed Trotsky's trip from New York to Russia. He was a major contributor to Woodrow Wilson's presidential campaign and an advocate for passage of the Federal Reserve Act. (p. 210) |

During the two years of hostilities thousands of Russian soldiers and sailors were taken as prisoners. Sources outside of Russia, which were hostile to the Tsarist regime, paid for the printing of Marxist propaganda and had it delivered to the prison camps. Russian-speaking revolutionaries were trained in New York and sent to distribute the pamphlets among the prisoners and to indoctrinate them into rebellion against their own government. When the war was ended, these officers and enlisted men returned home to become virtual seeds of treason against the Tsar. They were to play a major role a few years later in creating mutiny among the military during the Communist takeover of Russia.

TROTSKY WAS A MULTIPLE AGENT

One of the best known Russian revolutionaries at that time was Leon Trotsky. In January of 1916 Trotsky was expelled from France and came to the United States. It has been claimed that his expenses were paid by Jacob Schiff. There is no documentation to substantiate that claim, but the circumstantial evidence does point to a wealthy donor in New York. He remained for several months, while writing for a Russian socialist paper, the Novy Mir (New World) and giving revolutionary speeches at mass meetings in New York City. According to Trotsky himself, on many occasions a chauffeured limousine was placed at his service by a wealthy friend, identified as Dr. M. In his book, My Life, Trotsky wrote:

The doctor's wife took my wife and the boys out driving and was very kind to them. But she was a mere mortal, whereas the chauffeur was a magician, a titan, a superman! With the wave of his hand he made the machine obey his slightest command. To sit beside him was the supreme delight. When they went into a tea room, the boys would anxiously demand of their mother, "Why doesn't the chauffeur come in?" (Leon Trotsky: My Life, New York publisher: Scribner's, 1930, p. 277)

It must have been a curious sight to see the family of the great socialist radical, defender of the working class, enemy of capitalism, enjoying the pleasures of tea rooms and chauffeurs, the very symbols of capitalist luxury.

On March 23, 1917 a mass meeting was held at Carnegie Hall to celebrate the abdication of Nicolas II, which meant the overthrow of Tsarist rule in Russia. Thousands of socialists, Marxists, nihilists and anarchists attended to cheer the event. The following day there was published on page two of the New York Times a telegram from Jacob Schiff, which had been read to this audience. He expressed regrets, that he could not attend and then described the successful Russian revolution as "...what we had hoped and striven for these long years". (Mayor Calls Pacifists Traitors, The New York Times, March 24, 1917, p. 2)

In the February 3, 1949 issue of the New York Journal American Schiff's grandson, John, was quoted by columnist Cholly Knickerbocker as saying that his grandfather had given about $22 million for the triumph of Communism in Russia. (To appraise Schiff's motives for supporting the Bolsheviks, we must remember, that he was a Jew and that Russian Jews had been persecuted under the Tsarist regime. Consequently the Jewish community in America was inclined to support any movement, which sought to topple the Russian government and the Bolsheviks were excellent candidates for the task. As we shall see further along, however, there were also strong financial incentives for Wall Street firms, such as Kuhn, Loeb and Company, of which Schiff was a senior partner, to see the old regime fall into the hands of revolutionaries, who would agree to grant lucrative business concessions in the future in return for financial support today.)

When Trotsky returned to Petrograd in May of 1917 to organize the Bolshevik phase of the Russian Revolution, he carried $10,000 for travel expenses, a generously ample fund considering the value of the dollar at that time. Trotsky was arrested by Canadian and British naval personnel, when the ship, on which he was traveling, the S.S. Kristianiafjord, put in at Halifax. The money in his possession is now a matter of official record. The source of that money has been the focus of much speculation, but the evidence strongly suggests, that its origin was the German government. It was a sound investment.

Trotsky was not arrested on a whim. He was recognized as a threat to the best interests of England, Canada's mother country in the British Commonwealth. Russia was an ally of England in the First World War, which then was raging in Europe. Anything, that would weaken Russia - and that certainly included internal revolution - would be, in effect, to strengthen Germany and weaken England. In New York on the night before his departure Trotsky had given a speech, in which he said: "I am going back to Russia to overthrow the provisional government and stop the war with Germany." (A full report on this meeting had been submitted to the U.S. Military Intelligence. See Senate Document No. 62, 66th Congress, Report and Hearings of the Subcommittee on the Judiciary, United States Senate, 1919, Vol. II, p. 2680.) Trotsky therefore represented a real threat to England's war effort. He was arrested as a German agent and taken as a prisoner of war.

With this in mind we can appreciate the great strength of those mysterious forces both in England and the United States, that intervened on Trotsky's behalf. Immediately telegrams began to come into Halifax from such divergent sources, as an obscure attorney in New York City, from the Canadian Deputy Postmaster-General and even from a high-ranking British military officer, all inquiring into Trotsky's situation and urging his immediate release. The head of the British Secret Service in America at the time was Sir William Wiseman, who, as fate would have it, occupied the apartment directly above the apartment of Edward Mandell House and who had become fast friends with him. House advised Wiseman, that President Wilson wished to have Trotsky released. Wiseman advised his government and the British Admiralty issued orders on April 21st, that Trotsky was to be sent on his way. ("Why Did We Let Trotsky Go? How Canada Lost an Opportunity to Shorten the War", MacLeans magazine, Canada, June 1919. Also see Martin, pp. 163-164.) It was a fateful decision, that would affect not only the outcome of the war, but the future of the entire world.

It would be a mistake to conclude, that Jacob Schiff and Germany were the only players in this drama. Trotsky could not have gone even as far as Halifax without having been granted an American passport and this was accomplished by the personal intervention of President Wilson. Professor Antony Sutton says:

President Woodrow Wilson was the fairy godmother, who provided Trotsky with a passport to return to Russia to "carry forward" the revolution... At the same time careful State Department bureaucrats, concerned about such revolutionaries entering Russia, were unilaterally attempting to tighten up passport procedures. (Antony C. Sutton, Ph. D.: Wall Street and the Bolshevik Revolution, published by Arlington House in New Rochelle, NY, 1974, p. 25)

And there were others, as well. In 1911 the St. Louis Dispatch published a cartoon by a Bolshevik named Robert Minor. Minor was later to be arrested in Tsarist Russia for revolutionary activities and in fact was himself bankrolled by famous Wall Street financiers. Since we may safely assume, that he knew his topic well, his cartoon is of great historical importance. It portrays Karl Marx with a book entitled Socialism under his arm, standing amid a cheering crowd on Wall Street. Gathered around and greeting him with enthusiastic handshakes are characters in silk hats identified as John D. Rockefeller, J.P. Morgan, John D. Ryan of National City Bank, Morgan partner George W. Perkins and Teddy Roosevelt, leader of the Progressive Party.

This cartoon by Robert Minor appeared in the St. Louis Post-Dispatch in 1911. It shows Karl

Marx surrounded by enthusiastic Wall Street financiers: Morgan partner George Perkins,

J.P. Morgan, John Ryan of National City Bank, John D. Rockefeller and Andrew Carnegie.

Immediately behind Marx is Teddy Roosevelt, leader of the Progressive Party. (p. 211)

What emerges from this sampling of events is a clear pattern of strong support for Bolshevism coming from the highest financial and political power centers in the United States; from men, who supposedly were "capitalists" and who according to conventional wisdom should have been the mortal enemies of socialism and communism.

Nor was this phenomenon confined to the United States. Trotsky in his book My Life tells of a British financier, who in 1907 gave him a "large loan" to be repaid after the overthrow of the Tsar. Arsene de Goulevitch, who witnessed the Bolshevik Revolution firsthand, has identified both the name of the financier and the amount of the loan. "In private interviews", he said, "I have been told that over 21 million rubles were spent by Lord [Alfred] Milner in financing the Russian Revolution... The financier just mentioned was by no means alone among the British to support the Russian revolution with large financial donations." Another name specifically mentioned by de Goulevitch was that of Sir George Buchanan, the British Ambassador to Russia at the time. (See Arsene de Goulevitch: Czarism and Revolution, published by Omni Publications in Hawthorne, California, no date; rpt. from 1962 French edition, pp. 224, 230)

It was one thing for Americans to undermine Tsarist Russia and thus indirectly help Germany in the war, because American were not then into it, but for British citizens to do so was tantamount to treason. To understand, what higher loyalty compelled these men to betray their battlefield ally and to sacrifice the blood of their own countrymen, we must take a look at the unique organization, to which they belonged.

Pages 274-277: ROUND TABLE AGENTS IN RUSSIA

In Russia prior to and during the revolution there were many local observers, tourists and newsmen, who reported, that British and American agents were everywhere, particularly in Petrograd, providing money for insurrection. On report said, for example, that British agents were seen handing out 25-rouble notes to the men at the Pavlovski regiment just a few hours, before it mutinied against its officers and sided with the revolution. The subsequent publication of various memoirs and documents made it clear, that this funding was provided by Milner and channeled through Sir George Buchanan, who was the British Ambassador to Russia at the time. (See de Goulevitch, p. 230) It was a repeat of the ploy, that had worked so well for the cabal many times in the past. Round Table members were once again working both sides of the conflict to weaken and topple a target government. Tsar Nicholas had every reason to believe, that since the British were Russia's allies in the war against Germany, British officials would be the last persons on Earth to conspire against him. Yet the British Ambassador himself represented the hidden group, which was financing the regime's downfall.

The Round Table Agents from America did not have the advantage of using the diplomatic service as cover and therefore had to be considerably more ingenious. They came not as diplomats or even as interested businessmen, but disguised as Red Cross officials on a humanitarian mission. The group consisted almost entirely of financiers, lawyers and accountants from New York banks and investment houses. They simply had overpowered the American Red Cross organization with large contributions and in effect purchased a franchise to operate in its name. Professor Sutton tells us:

The 1910 [Red Cross] fund-raising campaign for $2 million, for example, was successful only, because it was supported by these wealthy residents of New York City. J.P. Morgan himself contributed $100,000... Henry P. Davison [a Morgan partner] was chairman of the 1910 New York Fund-Raising Committee and later became chairman of the War Council of the American Red Cross... The Red Cross was unable to cope with the demands of World War I. and in effect was taken over by these New York bankers. (Sutton: Revolution, p. 72)

For the duration of the war the Red Cross had been made nominally a part of the armed forces and subject to orders from the proper military authorities. It was not clear, who these authorities were and in fact there were never any orders, but the arrangement made it possible for the participants to receive military commissions and wear the uniform of American army officers. The entire expense of the Red Cross Mission in Russia, including the purchase of uniforms, was paid for by the man, who was appointed by President Wilson to become its head, "Colonel" William Boyce Thompson.

Thompson was a classical specimen of the Round Table network. Having begun his career as a speculator in copper mines, he soon moved into the world of high finance. He

- refinanced the American Woolen Company and the Tobacco Products Company;

- launched the Cuban Cane Sugar Company;

- purchased controlling interest in the Pierce Arrow Motor Car Company;

- organized the Submarine Boat Corporation and the Wright-Martin Aeroplane Company;

- became a director of the Chicago Rock Island & Pacific Railway, the Magma Arizona Railroad and the Metropolitan Life Insurance Company;

- was one of the heaviest stockholders in the Chase National Bank;

- was the agent for J.P. Morgan's British securities operation;

- became the first full-time director of the Federal Reserve Bank of New York, the most important bank in the Federal Reserve System;

- and of course contributed a quarter-million dollars to the Red Cross.

When Thompson arrived in Russia, he made it clear, that he was not your typical Red Cross representative. According to Hermann Hagedorn, Thompson's biographer:

He deliberately created the kind of setting, which would be expected of an American magnate: established himself in a suite in the Hotel de l'Europe, bought a French limousine, went dutifully to receptions and teas and evinced an interest in objects of art. Society and the diplomats, noting that here was a man of parts and power, began to flock about him. He was entertained at the embassies, at the houses of Kerensky's ministers. It was discovered, that he was a collector and those with antiques to sell fluttered around him offering him miniatures, Dresden china, tapestries, even a palace or two. (Hermann Hagedorn: The Magnate: William Boyce Thompson and His Time, published by Reynal & Hitchcock, New York, 1935, pp. 192-93)

When Thompson attended the opera, he was given the imperial box. People on the street called him the American Tsar. And it is not surprising, that according to George Kennan, "He was viewed by the Kerensky authorities as the 'real' ambassador of the United States." (George F. Kennan: Russia Leaves the War: Soviet-American Relations, 1917-1920 published by Princeton University Press in Princeton, NJ, 1956, p. 60)

It is now a matter of record, that Thompson syndicated the purchase on Wall Street of Russian bonds in the amount of ten million roubles. (Hagedorn, p. 192) In addition, he gave over two million roubles to Aleksandr Kerensky for propaganda purposes inside Russia and with J.P. Morgan gave the rouble equivalent of one million dollars to the Bolsheviks for the spreading of revolutionary propaganda outside of Russia, particularly in Germany and Austria. (Sutton: Revolution, pp. 83, 91.) It was the agitation made possible by this funding, that led to the abortive German Spartacus Revolt of 1918. (See article "W.B. Thompson, Red Cross Donor, Believes Party Misrepresented" in the Washington Post of Feb. 2, 1918) A photograph of the cablegram from Morgan to Thompson advising, that the money had been transferred to the National City Bank branch in Petrograd, is included in this book.

AN OBJECT LESSON IN SOUTH AFRICA

At first it may seem incongruous, that the Morgan group would provide funding for both Kerensky and Lenin. These men may have both been socialist revolutionaries, but they were miles apart in their plans for the future and in fact were bitter competitors for control of the new government. But the tactic of funding both sides in a political contest by then had been refined by members of the Round Table into a fine art. A stunning example of this occurred in South Africa during the outset of the Boer War in 1899.

- You are here:

-

Home

- Articles