Bitter Pill: Why Medical Bills Are Killing Us

- By Steven Brill - TIME Magazine - February 26, 2013

1. Routine Care, Unforgettable Bills

When Sean Recchi, a 42-year-old from Lancaster, Ohio, was told last March that he had non-Hodgkin’s lymphoma, his wife Stephanie knew she had to get him to MD Anderson Cancer Center in Houston. Stephanie’s father had been treated there 10 years earlier, and she and her family credited the doctors and nurses at MD Anderson with extending his life by at least eight years.

When Sean Recchi, a 42-year-old from Lancaster, Ohio, was told last March that he had non-Hodgkin’s lymphoma, his wife Stephanie knew she had to get him to MD Anderson Cancer Center in Houston. Stephanie’s father had been treated there 10 years earlier, and she and her family credited the doctors and nurses at MD Anderson with extending his life by at least eight years.

Because Stephanie and her husband had recently started their own small technology business, they were unable to buy comprehensive health insurance. For $469 a month, or about 20% of their income, they had been able to get only a policy that covered just $2,000 per day of any hospital costs. “We don’t take that kind of discount insurance,” said the woman at MD Anderson when Stephanie called to make an appointment for Sean.

Stephanie was then told by a billing clerk that the estimated cost of Sean’s visit — just to be examined for six days so a treatment plan could be devised — would be $48,900, due in advance. Stephanie got her mother to write her a check. “You do anything you can in a situation like that,” she says. The Recchis flew to Houston, leaving Stephanie’s mother to care for their two teenage children.

About a week later, Stephanie had to ask her mother for $35,000 more so Sean could begin the treatment the doctors had decided was urgent. His condition had worsened rapidly since he had arrived in Houston. He was “sweating and shaking with chills and pains,” Stephanie recalls. “He had a large mass in his chest that was … growing. He was panicked.”

Nonetheless, Sean was held for about 90 minutes in a reception area, she says, because the hospital could not confirm that the check had cleared. Sean was allowed to see the doctor only after he advanced MD Anderson $7,500 from his credit card. The hospital says there was nothing unusual about how Sean was kept waiting. According to MD Anderson communications manager Julie Penne, “Asking for advance payment for services is a common, if unfortunate, situation that confronts hospitals all over the United States.”

|

|

Claudia Susana for TIME Sean Recchi |

The total cost, in advance, for Sean to get his treatment plan and initial doses of chemotherapy was $83,900.

Why?

The first of the 344 lines printed out across eight pages of his hospital bill — filled with indecipherable numerical codes and acronyms — seemed innocuous. But it set the tone for all that followed. It read, “1 ACETAMINOPHE TABS 325 MG.” The charge was only $1.50, but it was for a generic version of a Tylenol pill. You can buy 100 of them on Amazon for $1.49 even without a hospital’s purchasing power.

(In-Depth Video: The Exorbitant Prices of Health Care)

Dozens of midpriced items were embedded with similarly aggressive markups, like $283.00 for a “CHEST, PA AND LAT 71020.” That’s a simple chest X-ray, for which MD Anderson is routinely paid $20.44 when it treats a patient on Medicare, the government health care program for the elderly.

Every time a nurse drew blood, a “ROUTINE VENIPUNCTURE” charge of $36.00 appeared, accompanied by charges of $23 to $78 for each of a dozen or more lab analyses performed on the blood sample. In all, the charges for blood and other lab tests done on Recchi amounted to more than $15,000. Had Recchi been old enough for Medicare, MD Anderson would have been paid a few hundred dollars for all those tests. By law, Medicare’s payments approximate a hospital’s cost of providing a service, including overhead, equipment and salaries.

On the second page of the bill, the markups got bolder. Recchi was charged $13,702 for “1 RITUXIMAB INJ 660 MG.” That’s an injection of 660 mg of a cancer wonder drug called Rituxan. The average price paid by all hospitals for this dose is about $4,000, but MD Anderson probably gets a volume discount that would make its cost $3,000 to $3,500. That means the nonprofit cancer center’s paid-in-advance markup on Recchi’s lifesaving shot would be about 400%.

When I asked MD Anderson to comment on the charges on Recchi’s bill, the cancer center released a written statement that said in part, “The issues related to health care finance are complex for patients, health care providers, payers and government entities alike … MD Anderson’s clinical billing and collection practices are similar to those of other major hospitals and academic medical centers.”

The hospital’s hard-nosed approach pays off. Although it is officially a nonprofit unit of the University of Texas, MD Anderson has revenue that exceeds the cost of the world-class care it provides by so much that its operating profit for the fiscal year 2010, the most recent annual report it filed with the U.S. Department of Health and Human Services, was $531 million. That’s a profit margin of 26% on revenue of $2.05 billion, an astounding result for such a service-intensive enterprise.1

The president of MD Anderson is paid like someone running a prosperous business. Ronald DePinho’s total compensation last year was $1,845,000. That does not count outside earnings derived from a much publicized waiver he received from the university that, according to the Houston Chronicle, allows him to maintain unspecified “financial ties with his three principal pharmaceutical companies.”

DePinho’s salary is nearly two and a half times the $750,000 paid to Francisco Cigarroa, the chancellor of entire University of Texas system, of which MD Anderson is a part. This pay structure is emblematic of American medical economics and is reflected on campuses across the U.S., where the president of a hospital or hospital system associated with a university — whether it’s Texas, Stanford, Duke or Yale — is invariably paid much more than the person in charge of the university.

I got the idea for this article when I was visiting Rice University last year. As I was leaving the campus, which is just outside the central business district of Houston, I noticed a group of glass skyscrapers about a mile away lighting up the evening sky. The scene looked like Dubai. I was looking at the Texas Medical Center, a nearly 1,300-acre, 280-building complex of hospitals and related medical facilities, of which MD Anderson is the lead brand name. Medicine had obviously become a huge business. In fact, of Houston’s top 10 employers, five are hospitals, including MD Anderson with 19,000 employees; three, led by ExxonMobil with 14,000 employees, are energy companies. How did that happen, I wondered. Where’s all that money coming from? And where is it going? I have spent the past seven months trying to find out by analyzing a variety of bills from hospitals like MD Anderson, doctors, drug companies and every other player in the American health care ecosystem.

When you look behind the bills that Sean Recchi and other patients receive, you see nothing rational — no rhyme or reason — about the costs they faced in a marketplace they enter through no choice of their own. The only constant is the sticker shock for the patients who are asked to pay.

(iReport: Tell Us Your Health Care Story)

|

|

Photograph by Nick Veasey for TIME Gauze Pads: $77 |

Yet those who work in the health care industry and those who argue over health care policy seem inured to the shock. When we debate health care policy, we seem to jump right to the issue of who should pay the bills, blowing past what should be the first question: Why exactly are the bills so high?

What are the reasons, good or bad, that cancer means a half-million- or million-dollar tab? Why should a trip to the emergency room for chest pains that turn out to be indigestion bring a bill that can exceed the cost of a semester of college? What makes a single dose of even the most wonderful wonder drug cost thousands of dollars? Why does simple lab work done during a few days in a hospital cost more than a car? And what is so different about the medical ecosystem that causes technology advances to drive bills up instead of down?

Recchi’s bill and six others examined line by line for this article offer a closeup window into what happens when powerless buyers — whether they are people like Recchi or big health-insurance companies — meet sellers in what is the ultimate seller’s market.

The result is a uniquely American gold rush for those who provide everything from wonder drugs to canes to high-tech implants to CT scans to hospital bill-coding and collection services. In hundreds of small and midsize cities across the country — from Stamford, Conn., to Marlton, N.J., to Oklahoma City — the American health care market has transformed tax-exempt “nonprofit” hospitals into the towns’ most profitable businesses and largest employers, often presided over by the regions’ most richly compensated executives. And in our largest cities, the system offers lavish paychecks even to midlevel hospital managers, like the 14 administrators at New York City’s Memorial Sloan-Kettering Cancer Center who are paid over $500,000 a year, including six who make over $1 million.

Taken as a whole, these powerful institutions and the bills they churn out dominate the nation’s economy and put demands on taxpayers to a degree unequaled anywhere else on earth. In the U.S., people spend almost 20% of the gross domestic product on health care, compared with about half that in most developed countries. Yet in every measurable way, the results our health care system produces are no better and often worse than the outcomes in those countries.

According to one of a series of exhaustive studies done by the McKinsey & Co. consulting firm, we spend more on health care than the next 10 biggest spenders combined: Japan, Germany, France, China, the U.K., Italy, Canada, Brazil, Spain and Australia. We may be shocked at the $60 billion price tag for cleaning up after Hurricane Sandy. We spent almost that much last week on health care. We spend more every year on artificial knees and hips than what Hollywood collects at the box office. We spend two or three times that much on durable medical devices like canes and wheelchairs, in part because a heavily lobbied Congress forces Medicare to pay 25% to 75% more for this equipment than it would cost at Walmart.

The Bureau of Labor Statistics projects that 10 of the 20 occupations that will grow the fastest in the U.S. by 2020 are related to health care. America’s largest city may be commonly thought of as the world’s financial-services capital, but of New York’s 18 largest private employers, eight are hospitals and four are banks. Employing all those people in the cause of curing the sick is, of course, not anything to be ashamed of. But the drag on our overall economy that comes with taxpayers, employers and consumers spending so much more than is spent in any other country for the same product is unsustainable. Health care is eating away at our economy and our treasury.

The health care industry seems to have the will and the means to keep it that way. According to the Center for Responsive Politics, the pharmaceutical and health-care-product industries, combined with organizations representing doctors, hospitals, nursing homes, health services and HMOs, have spent $5.36 billion since 1998 on lobbying in Washington. That dwarfs the $1.53 billion spent by the defense and aerospace industries and the $1.3 billion spent by oil and gas interests over the same period. That’s right: the health-care-industrial complex spends more than three times what the military-industrial complex spends in Washington.

SOUND OFF: Are Medical Bills Too High? Tell Us Why

When you crunch data compiled by McKinsey and other researchers, the big picture looks like this: We’re likely to spend $2.8 trillion this year on health care. That $2.8 trillion is likely to be $750 billion, or 27%, more than we would spend if we spent the same per capita as other developed countries, even after adjusting for the relatively high per capita income in the U.S. vs. those other countries. Of the total $2.8 trillion that will be spent on health care, about $800 billion will be paid by the federal government through the Medicare insurance program for the disabled and those 65 and older and the Medicaid program, which provides care for the poor. That $800 billion, which keeps rising far faster than inflation and the gross domestic product, is what’s driving the federal deficit. The other $2 trillion will be paid mostly by private health-insurance companies and individuals who have no insurance or who will pay some portion of the bills covered by their insurance. This is what’s increasingly burdening businesses that pay for their employees’ health insurance and forcing individuals to pay so much in out-of-pocket expenses.

1. Here and elsewhere I define operating profit as the hospital’s excess of revenue over expenses, plus the amount it lists on its tax return for depreciation of assets—because depreciation is an accounting expense, not a cash expense. John Gunn, chief operating officer of Memorial Sloan-Kettering Cancer Center, calls this the “fairest way” of judging a hospital’s financial performance

The original version of this article misidentified William Powers Jr., the president of the University of Texas system, as the head of the entire system. That is in fact Francisco Cigarroa, the chancellor of the University of Texas

Breaking these trillions down into real bills going to real patients cuts through the ideological debate over health care policy. By dissecting the bills that people like Sean Recchi face, we can see exactly how and why we are overspending, where the money is going and how to get it back. We just have to follow the money.

The $21,000 Heartburn Bill

One night last summer at her home near Stamford, Conn., a 64-year-old former sales clerk whom I’ll call Janice S. felt chest pains. She was taken four miles by ambulance to the emergency room at Stamford Hospital, officially a nonprofit institution. After about three hours of tests and some brief encounters with a doctor, she was told she had indigestion and sent home. That was the good news.

The bad news was the bill: $995 for the ambulance ride, $3,000 for the doctors and $17,000 for the hospital — in sum, $21,000 for a false alarm.

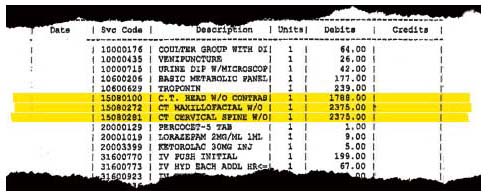

Out of work for a year, Janice S. had no insurance. Among the hospital’s charges were three “TROPONIN I” tests for $199.50 each. According to a National Institutes of Health website, a troponin test “measures the levels of certain proteins in the blood” whose release from the heart is a strong indicator of a heart attack. Some labs like to have the test done at intervals, so the fact that Janice S. got three of them is not necessarily an issue. The price is the problem. Stamford Hospital spokesman Scott Orstad told me that the $199.50 figure for the troponin test was taken from what he called the hospital’s chargemaster. The chargemaster, I learned, is every hospital’s internal price list. Decades ago it was a document the size of a phone book; now it’s a massive computer file, thousands of items long, maintained by every hospital.

Stamford Hospital’s chargemaster assigns prices to everything, including Janice S.’s blood tests. It would seem to be an important document. However, I quickly found that although every hospital has a chargemaster, officials treat it as if it were an eccentric uncle living in the attic. Whenever I asked, they deflected all conversation away from it. They even argued that it is irrelevant. I soon found that they have good reason to hope that outsiders pay no attention to the chargemaster or the process that produces it. For there seems to be no process, no rationale, behind the core document that is the basis for hundreds of billions of dollars in health care bills.

(VIDEO: The Exorbitant Prices of Health Care)

Because she was 64, not 65, Janice S. was not on Medicare. But seeing what Medicare would have paid Stamford Hospital for the troponin test if she had been a year older shines a bright light on the role the chargemaster plays in our national medical crisis — and helps us understand the illegitimacy of that $199.50 charge. That’s because Medicare collects troves of data on what every type of treatment, test and other service costs hospitals to deliver. Medicare takes seriously the notion that nonprofit hospitals should be paid for all their costs but actually be nonprofit after their calculation. Thus, under the law, Medicare is supposed to reimburse hospitals for any given service, factoring in not only direct costs but also allocated expenses such as overhead, capital expenses, executive salaries, insurance, differences in regional costs of living and even the education of medical students.

It turns out that Medicare would have paid Stamford $13.94 for each troponin test rather than the $199.50 Janice S. was charged.

Janice S. was also charged $157.61 for a CBC — the complete blood count that those of us who are ER aficionados remember George Clooney ordering several times a night. Medicare pays $11.02 for a CBC in Connecticut. Hospital finance people argue vehemently that Medicare doesn’t pay enough and that they lose as much as 10% on an average Medicare patient. But even if the Medicare price should be, say, 10% higher, it’s a long way from $11.02 plus 10% to $157.61. Yes, every hospital administrator grouses about Medicare’s payment rates — rates that are supervised by a Congress that is heavily lobbied by the American Hospital Association, which spent $1,859,041 on lobbyists in 2012. But an annual expense report that Stamford Hospital is required to file with the federal Department of Health and Human Services offers evidence that Medicare’s rates for the services Janice S. received are on the mark. According to the hospital’s latest filing (covering 2010), its total expenses for laboratory work (like Janice S.’s blood tests) in the 12 months covered by the report were $27.5 million. Its total charges were $293.2 million. That means it charged about 11 times its costs. As we examine other bills, we’ll see that like Medicare patients, the large portion of hospital patients who have private health insurance also get discounts off the listed chargemaster figures, assuming the hospital and insurance company have negotiated to include the hospital in the insurer’s network of providers that its customers can use. The insurance discounts are not nearly as steep as the Medicare markdowns, which means that even the discounted insurance-company rates fuel profits at these officially nonprofit hospitals. Those profits are further boosted by payments from the tens of millions of patients who, like the unemployed Janice S., have no insurance or whose insurance does not apply because the patient has exceeded the coverage limits. These patients are asked to pay the chargemaster list prices.

If you are confused by the notion that those least able to pay are the ones singled out to pay the highest rates, welcome to the American medical marketplace.

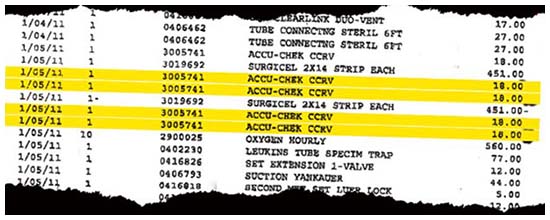

|

| Test Strips Patient was charged $18 each for Accu-chek diabetes test strips. Amazon sells boxes of 50 for about $27, or 55¢ each |

Pay No Attention To the Chargemaster

No hospital’s chargemaster prices are consistent with those of any other hospital, nor do they seem to be based on anything objective — like cost — that any hospital executive I spoke with was able to explain. “They were set in cement a long time ago and just keep going up almost automatically,” says one hospital chief financial officer with a shrug.

At Stamford Hospital I got the first of many brush-offs when I asked about the chargemaster rates on Janice S.’s bill. “Those are not our real rates,” protested hospital spokesman Orstad when I asked him to make hospital CEO Brian Grissler available to explain Janice S.’s bill, in particular the blood-test charges. “It’s a list we use internally in certain cases, but most people never pay those prices. I doubt that Brian [Grissler] has even seen the list in years. So I’m not sure why you care.”

Orstad also refused to comment on any of the specifics in Janice S.’s bill, including the seemingly inflated charges for all the lab work. “I’ve told you I don’t think a bill like this is relevant,” he explained. “Very few people actually pay those rates.”

But Janice S. was asked to pay them. Moreover, the chargemaster rates are relevant, even for those unlike her who have insurance. Insurers with the most leverage, because they have the most customers to offer a hospital that needs patients, will try to negotiate prices 30% to 50% above the Medicare rates rather than discounts off the sky-high chargemaster rates. But insurers are increasingly losing leverage because hospitals are consolidating by buying doctors’ practices and even rival hospitals. In that situation — in which the insurer needs the hospital more than the hospital needs the insurer — the pricing negotiation will be over discounts that work down from the chargemaster prices rather than up from what Medicare would pay. Getting a 50% or even 60% discount off the chargemaster price of an item that costs $13 and lists for $199.50 is still no bargain. “We hate to negotiate off of the chargemaster, but we have to do it a lot now,” says Edward Wardell, a lawyer for the giant health-insurance provider Aetna Inc.

That so few consumers seem to be aware of the chargemaster demonstrates how well the health care industry has steered the debate from why bills are so high to who should pay them.

The expensive technology deployed on Janice S. was a bigger factor in her bill than the lab tests. An “NM MYO REST/SPEC EJCT MOT MUL” was billed at $7,997.54. That’s a stress test using a radioactive dye that is tracked by an X-ray computed tomography, or CT, scan. Medicare would have paid Stamford $554 for that test.

Janice S. was charged an additional $872.44 just for the dye used in the test. The regular stress test patients are more familiar with, in which arteries are monitored electronically with an electrocardiograph, would have cost far less — $1,200 even at the hospital’s chargemaster price. (Medicare would have paid $96 for it.) And although many doctors view the version using the CT scan as more thorough, others consider it unnecessary in most cases.

According to Jack Lewin, a cardiologist and former CEO of the American College of Cardiology, “It depends on the patient, of course, but in most cases you would start with a standard stress test. We are doing too many of these nuclear tests. It is not being used appropriately … Sometimes a cardiogram is enough, and you don’t even need the simpler test. But it usually makes sense to give the patient the simpler one first and then use nuclear for a closer look if there seem to be problems.”

We don’t know the particulars of Janice S.’s condition, so we cannot know why the doctors who treated her ordered the more expensive test. But the incentives are clear. On the basis of market prices, Stamford probably paid about $250,000 for the CT equipment in its operating room. It costs little to operate, so the more it can be used and billed, the quicker the hospital recovers its costs and begins profiting from its purchase. In addition, the cardiologist in the emergency room gave Janice S. a separate bill for $600 to read the test results on top of the $342 he charged for examining her.

According to a McKinsey study of the medical marketplace, a typical piece of equipment will pay for itself in one year if it carries out just 10 to 15 procedures a day. That’s a terrific return on capital equipment that has an expected life span of seven to 10 years. And it means that after a year, every scan ordered by a doctor in the Stamford Hospital emergency room would mean pure profit, less maintenance costs, for the hospital. Plus an extra fee for the doctor.

Another McKinsey report found that health care providers in the U.S. conduct far more CT tests per capita than those in any other country — 71% more than in Germany, for example, where the government-run health care system offers none of those incentives for overtesting. We also pay a lot more for each test, even when it’s Medicare doing the paying. Medicare reimburses hospitals and clinics an average of four times as much as Germany does for CT scans, according to the data gathered by McKinsey.

Medicare’s reimbursement formulas for these tests are regulated by Congress. So too are restrictions on what Medicare can do to limit the use of CT and magnetic resonance imaging (MRI) scans when they might not be medically necessary. Standing at the ready to make sure Congress keeps Medicare at bay is, among other groups, the American College of Radiology, which on Nov. 14 ran a full-page ad in the Capitol Hill–centric newspaper Politico urging Congress to pass the Diagnostic Imaging Services Access Protection Act. It’s a bill that would block efforts by Medicare to discourage doctors from ordering multiple CT scans on the same patient by paying them less per test to read multiple tests of the same patient. (In fact, six of Politico’s 12 pages of ads that day were bought by medical interests urging Congress to spend or not cut back on one of their products.)

The costs associated with high-tech tests are likely to accelerate. McKinsey found that the more CT and MRI scanners are out there, the more doctors use them. In 1997 there were fewer than 3,000 machines available, and they completed an average of 3,800 scans per year. By 2006 there were more than 10,000 in use, and they completed an average of 6,100 per year. According to a study in the Annals of Emergency Medicine, the use of CT scans in America’s emergency rooms “has more than quadrupled in recent decades.” As one former emergency-room doctor puts it, “Giving out CT scans like candy in the ER is the equivalent of putting a 90-year-old grandmother through a pat-down at the airport: Hey, you never know.”

Selling this equipment to hospitals — which has become a key profit center for industrial conglomerates like General Electric and Siemens — is one of the U.S. economy’s bright spots. I recently subscribed to an online headhunter’s listings for medical-equipment salesmen and quickly found an opening in Connecticut that would pay a salary of $85,000 and sales commissions of up to $95,000 more, plus a car allowance. The only requirement was that applicants have “at least one year of experience selling some form of capital equipment.”

In all, on the day I signed up for that jobs website, it carried 186 listings for medical-equipment salespeople just in Connecticut.

SOUND OFF: Are Medical Bills Too High? Tell Us Why

2. Medical Technology’s Perverse Economics

Unlike those of almost any other area we can think of, the dynamics of the medical marketplace seem to be such that the advance of technology has made medical care more expensive, not less. First, it appears to encourage more procedures and treatment by making them easier and more convenient. (This is especially true for procedures like arthroscopic surgery.) Second, there is little patient pushback against higher costs because it seems to (and often does) result in safer, better care and because the customer getting the treatment is either not going to pay for it or not going to know the price until after the fact.

Beyond the hospitals’ and doctors’ obvious economic incentives to use the equipment and the manufacturers’ equally obvious incentives to sell it, there’s a legal incentive at work. Giving Janice S. a nuclear-imaging test instead of the lower-tech, less expensive stress test was the safer thing to do — a belt-and-suspenders approach that would let the hospital and doctor say they pulled out all the stops in case Janice S. died of a heart attack after she was sent home.

“We use the CT scan because it’s a great defense,” says the CEO of another hospital not far from Stamford. “For example, if anyone has fallen or done anything around their head — hell, if they even say the word head — we do it to be safe. We can’t be sued for doing too much.”

His rationale speaks to the real cost issue associated with medical-malpractice litigation. It’s not as much about the verdicts or settlements (or considerable malpractice-insurance premiums) that hospitals and doctors pay as it is about what they do to avoid being sued. And some no doubt claim they are ordering more tests to avoid being sued when it is actually an excuse for hiking profits. The most practical malpractice-reform proposals would not limit awards for victims but would allow doctors to use what’s called a safe-harbor defense. Under safe harbor, a defendant doctor or hospital could argue that the care provided was within the bounds of what peers have established as reasonable under the circumstances. The typical plaintiff argument that doing something more, like a nuclear-imaging test, might have saved the patient would then be less likely to prevail.

When Obamacare was being debated, Republicans pushed this kind of commonsense malpractice-tort reform. But the stranglehold that plaintiffs’ lawyers have traditionally had on Democrats prevailed, and neither a safe-harbor provision nor any other malpractice reform was included.

(iReport: Tell Us Your Health Care Story)

Nonprofit Profitmakers

To the extent that they defend the chargemaster rates at all, the defense that hospital executives offer has to do with charity. As John Gunn, chief operating officer of Sloan-Kettering, puts it, “We charge those rates so that when we get paid by a [wealthy] uninsured person from overseas, it allows us to serve the poor.”

A closer look at hospital finance suggests two holes in that argument. First, while Sloan-Kettering does have an aggressive financial-assistance program (something Stamford Hospital lacks), at most hospitals it’s not a Saudi sheik but the almost poor — those who don’t qualify for Medicaid and don’t have insurance — who are most often asked to pay those exorbitant chargemaster prices. Second, there is the jaw-dropping difference between those list prices and the hospitals’ costs, which enables these ostensibly nonprofit institutions to produce high profits even after all the discounts. True, when the discounts to Medicare and private insurers are applied, hospitals end up being paid a lot less overall than what is itemized on the original bills. Stamford ends up receiving about 35% of what it bills, which is the yield for most hospitals. (Sloan-Kettering and MD Anderson, whose great brand names make them tough negotiators with insurance companies, get about 50%). However, no matter how steep the discounts, the chargemaster prices are so high and so devoid of any calculation related to cost that the result is uniquely American: thousands of nonprofit institutions have morphed into high-profit, high-profile businesses that have the best of both worlds. They have become entities akin to low-risk, must-have public utilities that nonetheless pay their operators as if they were high-risk entrepreneurs. As with the local electric company, customers must have the product and can’t go elsewhere to buy it. They are steered to a hospital by their insurance companies or doctors (whose practices may have a business alliance with the hospital or even be owned by it). Or they end up there because there isn’t any local competition. But unlike with the electric company, no regulator caps hospital profits.

Yet hospitals are also beloved local charities.

The result is that in small towns and cities across the country, the local nonprofit hospital may be the community’s strongest business, typically making tens of millions of dollars a year and paying its nondoctor administrators six or seven figures. As nonprofits, such hospitals solicit contributions, and their annual charity dinner, a showcase for their good works, is typically a major civic event. But charitable gifts are a minor part of their base; Stamford Hospital raised just over 1% of its revenue from contributions last year. Even after discounts, those $199.50 blood tests and multithousand-dollar CT scans are what really count.

Thus, according to the latest publicly available tax return it filed with the IRS, for the fiscal year ending September 2011, Stamford Hospital — in a midsize city serving an unusually high 50% share of highly discounted Medicare and Medicaid patients — managed an operating profit of $63 million on revenue actually received (after all the discounts off the chargemaster) of $495 million. That’s a 12.7% operating profit margin, which would be the envy of shareholders of high-service businesses across other sectors of the economy.

Its nearly half-billion dollars in revenue also makes Stamford Hospital by far the city’s largest business serving only local residents. In fact, the hospital’s revenue exceeded all money paid to the city of Stamford in taxes and fees. The hospital is a bigger business than its host city.

There is nothing special about the hospital’s fortunes. Its operating profit margin is about the same as the average for all nonprofit hospitals, 11.7%, even when those that lose money are included. And Stamford’s 12.7% was tallied after the hospital paid a slew of high salaries to its management, including $744,000 to its chief financial officer and $1,860,000 to CEO Grissler.

In fact, when McKinsey, aided by a Bank of America survey, pulled together all hospital financial reports, it found that the 2,900 nonprofit hospitals across the country, which are exempt from income taxes, actually end up averaging higher operating profit margins than the 1,000 for-profit hospitals after the for-profits’ income-tax obligations are deducted. In health care, being nonprofit produces more profit.

Nonetheless, hospitals like Stamford are able to use their sympathetic nonprofit status to push their interests. As the debate over deficit-cutting ideas related to health care has heated up, the American Hospital Association has run daily ads on Mike Allen’s Playbook, a popular Washington tip sheet, urging that Congress not be allowed to cut hospital payments because that would endanger the “$39.3 billion” in uncompensated care for the poor that hospitals now provide either through charity programs or because of patients failing to pay their debts. Based on the formula hospitals use to calculate the cost of this charity care, that amounts to approximately 5% of their total revenue for 2010.

Under Internal Revenue Service rules, nonprofits are not prohibited from taking in more money than they spend. They just can’t distribute the overage to shareholders — because they don’t have any shareholders.

So, what do these wealthy nonprofits do with all the profit? In a trend similar to what we’ve seen in nonprofit colleges and universities — where there has been an arms race of sorts to use rising tuition to construct buildings and add courses of study — the hospitals improve and expand facilities (despite the fact that the U.S. has more hospital beds than it can fill), buy more equipment, hire more people, offer more services, buy rival hospitals and then raise executive salaries because their operations have gotten so much larger. They keep the upward spiral going by marketing for more patients, raising prices and pushing harder to collect bill payments. Only with health care, the upward spiral is easier to sustain. Health care is seen as even more of a necessity than higher education. And unlike in higher education, in health care there is little price transparency — and far less competition in any given locale even if there were transparency. Besides, a hospital is typically one of the community’s larger employers if not the largest, so there is unlikely to be much local complaining about its burgeoning economic fortunes.

In December, when the New York Times ran a story about how a deficit deal might threaten hospital payments, Steven Safyer, chief executive of Montefiore Medical Center, a large nonprofit hospital system in the Bronx, complained, “There is no such thing as a cut to a provider that isn’t a cut to a beneficiary … This is not crying wolf.”

Actually, Safyer seems to be crying wolf to the tune of about $196.8 million, according to the hospital’s latest publicly available tax return. That was his hospital’s operating profit, according to its 2010 return. With $2.586 billion in revenue — of which 99.4% came from patient bills and 0.6% from fundraising events and other charitable contributions — Safyer’s business is more than six times as large as that of the Bronx’s most famous enterprise, the New York Yankees. Surely, without cutting services to beneficiaries, Safyer could cut what have to be some of the Bronx’s better non-Yankee salaries: his own, which was $4,065,000, or those of his chief financial officer ($3,243,000), his executive vice president ($2,220,000) or the head of his dental department ($1,798,000).

Shocked by her bill from Stamford hospital and unable to pay it, Janice S. found a local woman on the Internet who is part of a growing cottage industry of people who call themselves medical-billing advocates. They help people read and understand their bills and try to reduce them. “The hospitals all know the bills are fiction, or at least only a place to start the discussion, so you bargain with them,” says Katalin Goencz, a former appeals coordinator in a hospital billing department who negotiated Janice S.’s bills from a home office in Stamford.

Goencz is part of a trade group called the Alliance of Claim Assistant Professionals, which has about 40 members across the country. Another group, Medical Billing Advocates of America, has about 50 members. Each advocate seems to handle 40 to 70 cases a year for the uninsured and those disputing insurance claims. That would be about 5,000 patients a year out of what must be tens of millions of Americans facing these issues — which may help explain why 60% of the personal bankruptcy filings each year are related to medical bills.

“I can pretty much always get it down 30% to 50% simply by saying the patient is ready to pay but will not pay $300 for a blood test or an X-ray,” says Goencz. “They hand out blood tests and X-rays in hospitals like bottled water, and they know it.”

After weeks of back-and-forth phone calls, for which Goencz charged Janice S. $97 an hour, Stamford Hospital cut its bill in half. Most of the doctors did about the same, reducing Janice S.’s overall tab from $21,000 to about $11,000.

But the best the ambulance company would offer Goencz was to let Janice S. pay off its $995 ride in $25-a-month installments. “The ambulances never negotiate the amount,” says Goencz.

A manager at Stamford Emergency Medical Services, which charged Janice S. $958 for the pickup plus $9.38 per mile, says that “our rates are all set by the state on a regional basis” and that the company is independently owned. That’s at odds with a trend toward consolidation that has seen several private-equity firms making investments in what Wall Street analysts have identified as an increasingly high-margin business. Overall, ambulance revenues were more than $12 billion last year, or about 10% higher than Hollywood’s box-office take. It’s not a great deal to pay off $1,000 for a four-mile ambulance ride on the layaway plan or receive a 50% discount on a $199.50 blood test that should cost $15, nor is getting half off on a $7,997.54 stress test that was probably all profit and may not have been necessary. But, says Goencz, “I don’t go over it line by line. I just go for a deal. The patient usually is shocked by the bill, doesn’t understand any of the language and has bill collectors all over her by the time they call me. So they’re grateful. Why give them heartache by telling them they still paid too much for some test or pill?”

SOUND OFF: Are Medical Bills Too High? Tell Us Why

The original version of this article stated that the total annual amount of charity care provided by U.S. hospitals cost them less than half of 1% of their annual revenue. In fact, the uncompensated care hospitals provide, either through charity programs or because of patients failing to pay their debts, amounts to approximately 5% of their total revenue for 2010.

A Slip, a Fall And a $9,400 Bill

The billing advocates aren’t always successful. just ask Emilia Gilbert, a school-bus driver who got into a fight with a hospital associated with Connecticut’s most venerable nonprofit institution, which racked up quick profits on multiple CT scans, then refused to compromise at all on its chargemaster prices. Gilbert, now 66, is still making weekly payments on the bill she got in June 2008 after she slipped and fell on her face one summer evening in the small yard behind her house in Fairfield, Conn. Her nose bleeding heavily, she was taken to the emergency room at Bridgeport Hospital.

Along with Greenwich Hospital and the Hospital of St. Raphael in New Haven, Bridgeport Hospital is now owned by the Yale New Haven Health System, which boasts a variety of gleaming new facilities. Although Yale University and Yale New Haven are separate entities, Yale–New Haven Hospital is the teaching hospital for the Yale Medical School, and university representatives, including Yale president Richard Levin, sit on the Yale New Haven Health System board.

“I was there for maybe six hours, until midnight,” Gilbert recalls, “and most of it was spent waiting. I saw the resident for maybe 15 minutes, but I got a lot of tests.”

In fact, Gilbert got three CT scans — of her head, her chest and her face. The last one showed a hairline fracture of her nose. The CT bills alone were $6,538. (Medicare would have paid about $825 for all three.) A doctor charged $261 to read the scans.

Gilbert got the same troponin blood test that Janice S. got — the one Medicare pays $13.94 for and for which Janice S. was billed $199.50 at Stamford. Gilbert got just one. Bridgeport Hospital charged 20% more than its downstate neighbor: $239.

Also on the bill were items that neither Medicare nor any insurance company would pay anything at all for: basic instruments and bandages and even the tubing for an IV setup. Under Medicare regulations and the terms of most insurance contracts, these are supposed to be part of the hospital’s facility charge, which in this case was $908 for the emergency room.

|

|

Javier Sirvent for TIME Emilia Gilbert |

Gilbert’s total bill was $9,418.

“We think the chargemaster is totally fair,” says William Gedge, senior vice president of payer relations at Yale New Haven Health System. “It’s fair because everyone gets the same bill. Even Medicare gets exactly the same charges that this patient got. Of course, we will have different arrangements for how Medicare or an insurance company will not pay some of the charges or discount the charges, but everyone starts from the same place.” Asked how the chargemaster charge for an item like the troponin test was calculated, Gedge said he “didn’t know exactly” but would try to find out. He subsequently reported back that “it’s an historical charge, which takes into account all of our costs for running the hospital.”

Bridgeport Hospital had $420 million in revenue and an operating profit of $52 million in 2010, the most recent year covered by its federal financial reports. CEO Robert Trefry, who has since left his post, was listed as having been paid $1.8 million. The CEO of the parent Yale New Haven Health System, Marna Borgstrom, was paid $2.5 million, which is 58% more than the $1.6 million paid to Levin, Yale University’s president.

“You really can’t compare the two jobs,” says Yale–New Haven Hospital senior vice president Vincent Petrini. “Comparing hospitals to universities is like apples and oranges. Running a hospital organization is much more complicated.” Actually, the four-hospital chain and the university have about the same operating budget. And it would seem that Levin deals with what most would consider complicated challenges in overseeing 3,900 faculty members, corralling (and complying with the terms of) hundreds of millions of dollars in government research grants and presiding over a $19 billion endowment, not to mention admitting and educating 14,000 students spread across Yale College and a variety of graduate schools, professional schools and foreign-study outposts. And surely Levin’s responsibilities are as complicated as those of the CEO of Yale New Haven Health’s smallest unit — the 184-bed Greenwich Hospital, whose CEO was paid $112,000 more than Levin.

“When I got the bill, I almost had to go back to the hospital,” Gilbert recalls. “I was hyperventilating.” Contributing to her shock was the fact that although her employer supplied insurance from Cigna, one of the country’s leading health insurers, Gilbert’s policy was from a Cigna subsidiary called Starbridge that insures mostly low-wage earners. That made Gilbert one of millions of Americans like Sean Recchi who are routinely categorized as having health insurance but really don’t have anything approaching meaningful coverage.

Starbridge covered Gilbert for just $2,500 per hospital visit, leaving her on the hook for about $7,000 of a $9,400 bill. Under Connecticut’s rules (states set their own guidelines for Medicaid, the federal-state program for the poor), Gilbert’s $1,800 a month in earnings was too high for her to qualify for Medicaid assistance. She was also turned down, she says, when she requested financial assistance from the hospital. Yale New Haven’s Gedge insists that she never applied to the hospital for aid, and Gilbert could not supply me with copies of any applications.

In September 2009, after a series of fruitless letters and phone calls from its bill collectors to Gilbert, the hospital sued her. Gilbert found a medical-billing advocate, Beth Morgan, who analyzed the charges on the bill and compared them with the discounted rates insurance companies would pay. During two court-required mediation sessions, Bridgeport Hospital’s attorney wouldn’t budge; his client wanted the bill paid in full, Gilbert and Morgan recall. At the third and final mediation, Gilbert was offered a 20% discount off the chargemaster fees if she would pay immediately, but she says she responded that according to what Morgan told her about the bill, it was still too much to pay. “We probably could have offered more,” Gedge acknowledges. “But in these situations, our bill-collection attorneys only know the amount we are saying is owed, not whether it is a chargemaster amount or an amount that is already discounted.”

On July 11, 2011, with the school-bus driver representing herself in Bridgeport superior court, a judge ruled that Gilbert had to pay all but about $500 of the original charges. (He deducted the superfluous bills for the basic equipment.) The judge put her on a payment schedule of $20 a week for six years. For her, the chargemaster prices were all too real.

The One-Day, $87,000 Outpatient Bill

Getting a patient in and out of a hospital the same day seems like a logical way to cut costs. Outpatients don’t take up hospital rooms or require the expensive 24/7 observation and care that come with them. That’s why in the 1990s Medicare pushed payment formulas on hospitals that paid them for whatever ailment they were treating (with more added for documented complications), not according to the number of days the patient spent in a bed. Insurance companies also pushed incentives on hospitals to move patients out faster or not admit them for overnight stays in the first place. Meanwhile, the introduction of procedures like noninvasive laparoscopic surgery helped speed the shift from inpatient to outpatient.

By 2010, average days spent in the hospital per patient had declined significantly, while outpatient services had increased even more dramatically. However, the result was not the savings that reformers had envisioned. It was just the opposite.

Experts estimate that outpatient services are now packed with so much hidden profit that about two-thirds of the $750 billion annual U.S. overspending identified by the McKinsey research on health care comes in payments for outpatient services. That includes work done by physicians, laboratories and clinics (including diagnostic clinics for CT scans or blood tests) and same-day surgeries and other hospital treatments like cancer chemotherapy. According to a McKinsey survey, outpatient emergency-room care averages an operating profit margin of 15% and nonemergency outpatient care averages 35%. On the other hand, inpatient care has a margin of just 2%. Put simply, inpatient care at nonprofit hospitals is, in fact, almost nonprofit. Outpatient care is wildly profitable.

“An operating room has fixed costs,” explains one hospital economist. “You get 10% or 20% more patients in there every day who you don’t have to board overnight, and that goes straight to the bottom line.”

The 2011 outpatient visit of someone I’ll call Steve H. to Mercy Hospital in Oklahoma City illustrates those economics. Steve H. had the kind of relatively routine care that patients might expect would be no big deal: he spent the day at Mercy getting his aching back fixed.

A blue collar worker who was in his 30s at the time and worked at a local retail store, Steve H. had consulted a specialist at Mercy in the summer of 2011 and was told that a stimulator would have to be surgically implanted in his back. The good news was that with all the advances of modern technology, the whole process could be done in a day. (The latest federal filing shows that 63% of surgeries at Mercy were performed on outpatients.)

Steve H.’s doctor intended to use a RestoreUltra neurostimulator manufactured by Medtronic, a Minneapolis-based company with $16 billion in annual sales that bills itself as the world’s largest stand-alone medical-technology company. “RestoreUltra delivers spinal-cord stimulation through one or more leads selected from a broad portfolio for greater customization of therapy,” Medtronic’s website promises. I was not able to interview Steve H., but according to Pat Palmer, a medical-billing specialist based in Salem, Va., who consults for the union that provides Steve H.’s health insurance, Steve H. didn’t ask how much the stimulator would cost because he had $45,181 remaining on the $60,000 annual payout limit his union-sponsored health-insurance plan imposed. “He figured, How much could a day at Mercy cost?” Palmer says. “Five thousand? Maybe 10?”

Steve H. was about to run up against a seemingly irrelevant footnote in millions of Americans’ insurance policies: the limit, sometimes annual or sometimes over a lifetime, on what the insurer has to pay out for a patient’s claims. Under Obamacare, those limits will not be allowed in most health-insurance policies after 2013. That might help people like Steve H. but is also one of the reasons premiums are going to skyrocket under Obamacare.

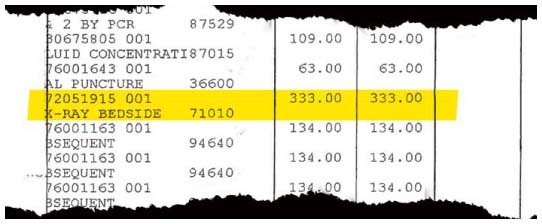

|

| Chest X-Ray Patient was charged $333. the national rate paid by Medicare is $23.83 |

Steve H.’s bill for his day at Mercy contained all the usual and customary overcharges. One item was “MARKER SKIN REG TIP RULER” for $3. That’s the marking pen, presumably reusable, that marked the place on Steve H.’s back where the incision was to go. Six lines down, there was “STRAP OR TABLE 8X27 IN” for $31. That’s the strap used to hold Steve H. onto the operating table. Just below that was “BLNKT WARM UPPER BDY 42268” for $32. That’s a blanket used to keep surgery patients warm. It is, of course, reusable, and it’s available new on eBay for $13. Four lines down there’s “GOWN SURG ULTRA XLG 95121” for $39, which is the gown the surgeon wore. Thirty of them can be bought online for $180. Neither Medicare nor any large insurance company would pay a hospital separately for those straps or the surgeon’s gown; that’s all supposed to come with the facility fee paid to the hospital, which in this case was $6,289.

In all, Steve H.’s bill for these basic medical and surgical supplies was $7,882. On top of that was $1,837 under a category called “Pharmacy General Classification” for items like bacitracin ($108). But that was the least of Steve H.’s problems.

The big-ticket item for Steve H.’s day at Mercy was the Medtronic stimulator, and that’s where most of Mercy’s profit was collected during his brief visit. The bill for that was $49,237.

According to the chief financial officer of another hospital, the wholesale list price of the Medtronic stimulator is “about $19,000.” Because Mercy is part of a major hospital chain, it might pay 5% to 15% less than that. Even assuming Mercy paid $19,000, it would make more than $30,000 selling it to Steve H., a profit margin of more than 150%. To the extent that I found any consistency among hospital chargemaster practices, this is one of them: hospitals routinely seem to charge 21⁄2 times what these expensive implantable devices cost them, which produces that 150% profit margin.

As Steve H. found out when he got his bill, he had exceeded the $45,000 that was left on his insurance policy’s annual payout limit just with the neurostimulator. And his total bill was $86,951. After his insurance paid that first $45,000, he still owed more than $40,000, not counting doctors’ bills. (I did not see Steve H.’s doctors’ bills.)

SOUND OFF: Are Medical Bills Too High? Tell Us Why

Mercy Hospital is owned by an organization under the umbrella of the Catholic Church called Sisters of Mercy. Its mission, as described in its latest filing with the IRS as a tax-exempt charity, is “to carry out the healing ministry of Jesus by promoting health and wellness.” With a chain of 31 hospitals and 300 clinics across the Midwest, Sisters of Mercy uses a bill-collection firm based in Topeka, Kans., called Berlin-Wheeler Inc. Suits against Mercy patients are on file in courts across Oklahoma listing Berlin-Wheeler as the plaintiff. According to its most recent tax return, the Oklahoma City unit of the Sisters of Mercy hospital chain collected $337 million in revenue for the fiscal year ending June 30, 2011. It had an operating profit of $34 million. And that was after paying 10 executives more than $300,000 each, including $784,000 to a regional president and $438,000 to the hospital president.

That report doesn’t cover the executives overseeing the chain, called Mercy Health, of which Mercy in Oklahoma City is a part. The overall chain had $4.28 billion in revenue that year. Its hospital in Springfield, Mo. (pop. 160,660), had $880.7 million in revenue and an operating profit of $319 million, according to its federal filing. The incomes of the parent company’s executives appear on other IRS filings covering various interlocking Mercy nonprofit corporate entities. Mercy president and CEO Lynn Britton made $1,930,000, and an executive vice president, Myra Aubuchon, was paid $3.7 million, according to the Mercy filing. In all, seven Mercy Health executives were paid more than $1 million each. A note at the end of an Ernst & Young audit that is attached to Mercy’s IRS filing reported that the chain provided charity care worth 3.2% of its revenue in the previous year. However, the auditors state that the value of that care is based on the charges on all the bills, not the actual cost to Mercy of providing those services — in other words, the chargemaster value. Assuming that Mercy’s actual costs are a tenth of these chargemaster values — they’re probably less — all of this charity care actually cost Mercy about three-tenths of 1% of its revenue, or about $13 million out of $4.28 billion.

Mercy’s website lists an 18-member media team; one member, Rachel Wright, told me that neither CEO Britton nor anyone else would be available to answer questions about compensation, the hospital’s bill-collecting activities through Berlin-Wheeler or Steve H.’s bill, which I had sent her (with his name and the date of his visit to the hospital redacted to protect his privacy).

|

|

Photograph by Nick Veasey for TIME Bacitracin: $108 |

Wright said the hospital’s lawyers had decided that discussing Steve H.’s bill would violate the federal HIPAA law protecting the privacy of patient medical records. I pointed out that I wanted to ask questions only about the hospital’s charges for standard items — such as surgical gowns, basic blood tests, blanket warmers and even medical devices — that had nothing to do with individual patients. “Everything is particular to an individual patient’s needs,” she replied. Even a surgical gown? “Yes, even a surgical gown. We cannot discuss this with you. It’s against the law.” She declined to put me in touch with the hospital’s lawyers to discuss their legal analysis.

Hiding behind a privacy statute to avoid talking about how it prices surgeons’ gowns may be a stretch, but Mercy might have a valid legal reason not to discuss what it paid for the Medtronic device before selling it to Steve H. for $49,237. Pharmaceutical and medical-device companies routinely insert clauses in their sales contracts prohibiting hospitals from sharing information about what they pay and the discounts they receive. In January 2012, a report by the federal Government Accountability Office found that “the lack of price transparency and the substantial variation in amounts hospitals pay for some IMD [implantable medical devices] raise questions about whether hospitals are achieving the best prices possible.”

A lack of price transparency was not the only potential market inefficiency the GAO found. “Although physicians are not involved in price negotiations, they often express strong preferences for certain manufacturers and models of IMD,” the GAO reported. “To the extent that physicians in the same hospitals have different preferences for IMDs, it may be difficult for the hospital to obtain volume discounts from particular manufacturers.”

“Doctors have no incentive to buy one kind of hip or other implantable device as a group,” explains Ezekiel Emanuel, an oncologist and a vice provost of the University of Pennsylvania who was a key White House adviser when Obamacare was created. “Even in the most innocent of circumstances, it kills the chance for market efficiencies.”

The circumstances are not always innocent. In 2008, Gregory Demske, an assistant inspector general at the Department of Health and Human Services, told a Senate committee that “physicians routinely receive substantial compensation from medical-device companies through stock options, royalty agreements, consulting agreements, research grants and fellowships.”

The assistant inspector general then revealed startling numbers about the extent of those payments: “We found that during the years 2002 through 2006, four manufacturers, which controlled almost 75% of the hip- and knee-replacement market, paid physician consultants over $800 million under the terms of roughly 6,500 consulting agreements.”

Other doctors, Demske noted, had stretched the conflict of interest beyond consulting fees: “Additionally, physician ownership of medical-device manufacturers and related businesses appears to be a growing trend in the medical-device sector … In some cases, physicians could receive substantial returns while contributing little to the venture beyond the ability to generate business for the venture.” In 2010, Medtronic, along with several other members of a medical-technology trade group, began to make the potential conflicts transparent by posting all payments to physicians on a section of its website called Physician Collaboration. The voluntary move came just before a similar disclosure regulation promulgated by the Obama Administration went into effect governing any doctor who receives funds from Medicare or the National Institutes of Health (which would include most doctors). And the nonprofit public-interest-journalism organization ProPublica has smartly organized data on doctor payments on its website. The conflicts have not been eliminated, but they are being aired, albeit on searchable websites rather than through a requirement that doctors disclose them to patients directly.

But conflicts that may encourage devices to be overprescribed or that lead doctors to prescribe a more expensive one instead of another are not the core problem in this marketplace. The more fundamental disconnect is that there is little reason to believe that what Mercy Hospital paid Medtronic for Steve H.’s device would have had any bearing on what the hospital decided to charge Steve H. Why would it? He did not know the price in advance.

Besides, studies delving into the economics of the medical marketplace consistently find that a moderately higher or lower price doesn’t change consumer purchasing decisions much, if at all, because in health care there is little of the price sensitivity found in conventional marketplaces, even on the rare occasion that patients know the cost in advance. If you were in pain or in danger of dying, would you turn down treatment at a price 5% or 20% higher than the price you might have expected — that is, if you’d had any informed way to know what to expect in the first place, which you didn’t?

The question of how sensitive patients will be to increased prices for medical devices recently came up in a different context. Aware of the huge profits being accumulated by devicemakers, Obama Administration officials decided to recapture some of the money by imposing a 2.39% federal excise tax on the sales of these devices as well as other medical technology such as CT-scan equipment. The rationale was that getting back some of these generous profits was a fair way to cover some of the cost of the subsidized, broader insurance coverage provided by Obamacare — insurance that in some cases will pay for more of the devices. The industry has since geared up in Washington and is pushing legislation that would repeal the tax. Its main argument is that a 2.39% increase in prices would so reduce sales that it would wipe out a substantial portion of what the industry claims are the 422,000 jobs it supports in a $136 billion industry.

That prediction of doom brought on by this small tax contradicts the reams of studies documenting consumer price insensitivity in the health care marketplace. It also ignores profit-margin data collected by McKinsey that demonstrates that devicemakers have an open field in the current medical ecosystem. A 2011 McKinsey survey for medical-industry clients reported that devicemakers are superstar performers in a booming medical economy. Medtronic, which performed in the middle of the group, delivered an amazing compounded annual return of 14.95% to shareholders from 1990 to 2010. That means $100 invested in the company in 1990 was worth $1,622 20 years later. So if the extra 2.39% would be so disruptive to the market for products like Medtronic’s that it would kill sales, why would the industry pass it along as a price increase to consumers? It hardly has to, given its profit margins.

Medtronic spokeswoman Donna Marquad says that for competitive reasons, her company will not discuss sales figures or the profit on Steve H.’s neurostimulator. But Medtronic’s October 2012 quarterly SEC filing reported that its spine “products and therapies,” which presumably include Steve H.’s device, “continue to gain broad surgeon acceptance” and that its cost to make all of its products was 24.9% of what it sells them for.

That’s an unusually high gross profit margin — 75.1% — for a company that manufactures real physical products. Apple also produces high-end, high-tech products, and its gross margin is 40%. If the neurostimulator enjoys that company-wide profit margin, it would mean that if Medtronic was paid $19,000 by Mercy Hospital, Medtronic’s cost was about $4,500 and it made a gross profit of about $14,500 before expenses for sales, overhead and management — including CEO Omar Ishrak’s compensation, which was $25 million for the 2012 fiscal year.

Mercy’s Bargain

When Pat Palmer, the medical-billing specialist who advises Steve H.’s union, was given the Mercy bill to deal with, she prepared a tally of about $4,000 worth of line items that she thought represented the most egregious charges, such as the surgical gown, the blanket warmer and the marking pen. She restricted her list to those she thought were plainly not allowable. “I didn’t dispute nearly all of them,” she says. “Because then they get their backs up.”

The hospital quickly conceded those items. For the remaining $83,000, Palmer invoked a 40% discount off chargemaster rates that Mercy allows for smaller insurance providers like the union. That cut the bill to about $50,000, for which the insurance company owed 80%, or about $40,000. That left Steve H. with a $10,000 bill.

Sean Recchi wasn’t as fortunate. His bill — which included not only the aggressively marked-up charge of $13,702 for the Rituxan cancer drug but also the usual array of chargemaster fees for basics like generic Tylenol, blood tests and simple supplies — had one item not found on any other bill I examined: MD Anderson’s charge of $7 each for “ALCOHOL PREP PAD.” This is a little square of cotton used to apply alcohol to an injection. A box of 200 can be bought online for $1.91.

We have seen that to the extent that most hospital administrators defend such chargemaster rates at all, they maintain that they are just starting points for a negotiation. But patients don’t typically know they are in a negotiation when they enter the hospital, nor do hospitals let them know that. And in any case, at MD Anderson, the Recchis were made to pay every penny of the chargemaster bill up front because their insurance was deemed inadequate. That left Penne, the hospital spokeswoman, with only this defense for the most blatantly abusive charges for items like the alcohol squares: “It is difficult to compare a retail store charge for a common product with a cancer center that provides the item as part of its highly specialized and personalized care,” she wrote in an e-mail. Yet the hospital also charges for that “specialized and personalized” care through, among other items, its $1,791-a-day room charge.

Before MD Anderson marked up Recchi’s Rituxan to $13,702, the profit taking was equally aggressive, and equally routine, at the beginning of the supply chain — at the drug company. Rituxan is a prime product of Biogen Idec, a company with $5.5 billion in annual sales. Its CEO, George Scangos, was paid $11,331,441 in 2011, a 20% boost over his 2010 income. Rituxan is made and sold by Biogen Idec in partnership with Genentech, a South San Francisco–based biotechnology pioneer. Genentech brags about Rituxan on its website, as did Roche, Genentech’s $45 billion parent, in its latest annual report. And in an Investor Day presentation last September, Roche CEO Severin Schwann stressed that his company is able to keep prices and margins high because of its focus on “medically differentiated therapies.” Rituxan, a cancer wonder drug, certainly meets that test.

SOUND OFF: Are Medical Bills Too High? Tell Us Why

A spokesman at Genentech for the Biogen Idec–Genentech partnership would not say what the drug cost the companies to make, but according to its latest annual report, Biogen Idec’s cost of sales — the incremental expense of producing and shipping each of its products compared with what it sells them for — was only 10%. That’s lower than the incremental cost of sales for most software companies, and the software companies usually don’t produce anything physical or have to pay to ship anything.

This would mean that Sean Recchi’s dose of Rituxan cost the Biogen Idec–Genentech partnership as little as $300 to make, test, package and ship to MD Anderson for $3,000 to $3,500, whereupon the hospital sold it to Recchi for $13,702.

As 2013 began, Recchi was being treated back in Ohio because he could not pay MD Anderson for more than his initial treatment. As for the $13,702-a-dose Rituxan, it turns out that Biogen Idec’s partner Genentech has a charity-access program that Recchi’s Ohio doctor told him about that enabled him to get those treatments free. “MD Anderson never said a word to us about the Genentech program,” says Stephanie Recchi. “They just took our money up front.”

Genentech spokeswoman Charlotte Arnold would not disclose how much free Rituxan had been dispensed to patients like Recchi in the past year, saying only that Genentech has “donated $2.85 billion in free medicine to uninsured patients in the U.S.” since 1985. That seems like a lot until the numbers are broken down. Arnold says the $2.85 billion is based on what the drugmaker sells the product for, not what it costs Genentech to make. On the basis of Genentech’s historic costs and revenue since 1985, that would make the cost of these donations less than 1% of Genentech’s sales — not something likely to take the sizzle out of CEO Severin’s Investor Day.

Nonetheless, the company provided more financial support than MD Anderson did to Recchi, whose wife reports that he “is doing great. He’s in remission.”

Penne of MD Anderson stressed that the hospital provides its own financial aid to patients but that the state legislature restricts the assistance to Texas residents. She also said MD Anderson “makes every attempt” to inform patients of drug-company charity programs and that 50 of the hospital’s 24,000 inpatients and outpatients, one of whom was from outside Texas, received charitable aid for Rituxan treatments in 2012.

3. Catastrophic Illness — And the Bills to Match

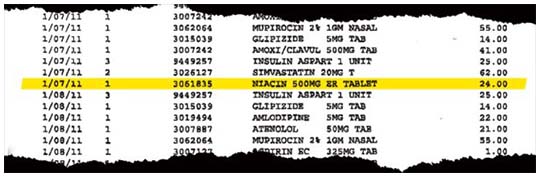

When medical care becomes a matter of life and death, the money demanded by the health care ecosystem reaches a wholly different order of magnitude, churning out reams of bills to people who can’t focus on them, let alone pay them. Soon after he was diagnosed with lung cancer in January 2011, a patient whom I will call Steven D. and his wife Alice knew that they were only buying time. The crushing question was, How much is time really worth? As Alice, who makes about $40,000 a year running a child-care center in her home, explained, “[Steven] kept saying he wanted every last minute he could get, no matter what. But I had to be thinking about the cost and how all this debt would leave me and my daughter.” By the time Steven D. died at his home in Northern California the following November, he had lived for an additional 11 months. And Alice had collected bills totaling $902,452. The family’s first bill — for $348,000 — which arrived when Steven got home from the Seton Medical Center in Daly City, Calif., was full of all the usual chargemaster profit grabs: $18 each for 88 diabetes-test strips that Amazon sells in boxes of 50 for $27.85; $24 each for 19 niacin pills that are sold in drugstores for about a nickel apiece. There were also four boxes of sterile gauze pads for $77 each. None of that was considered part of what was provided in return for Seton’s facility charge for the intensive-care unit for two days at $13,225 a day, 12 days in the critical unit at $7,315 a day and one day in a standard room (all of which totaled $120,116 over 15 days). There was also $20,886 for CT scans and $24,251 for lab work. Alice responded to my question about the obvious overcharges on the bill for items like the diabetes-test strips or the gauze pads much as Mrs. Lincoln, according to the famous joke, might have had she been asked what she thought of the play. “Are you kidding?” she said. “I’m dealing with a husband who had just been told he has Stage IV cancer. That’s all I can focus on … You think I looked at the items on the bills? I just looked at the total.”

Steven and Alice didn’t know that hospital billing people consider the chargemaster to be an opening bid. That’s because no medical bill ever says, “Give us your best offer.” The couple knew only that the bill said they had maxed out on the $50,000 payout limit on a UnitedHealthcare policy they had bought through a community college where Steven had briefly enrolled a year before. “We were in shock,” Alice recalls. “We looked at the total and couldn’t deal with it. So we just started putting all the bills in a box. We couldn’t bear to look at them.”

The $50,000 that UnitedHealthcare paid to Seton Medical Center was worth about $80,000 in credits because any charges covered by the insurer were subject to the discount it had negotiated with Seton. After that $80,000, Steven and Alice were on their own, not eligible for any more discounts. Four months into her husband’s illness, Alice by chance got the name of Patricia Stone, a billing advocate based in Menlo Park, Calif. Stone’s typical clients are middle-class people having trouble with insurance claims. Stone felt so bad for Steven and Alice — she saw the blizzard of bills Alice was going to have to sort through — that, says Alice, she “gave us many of her hours,” for which she usually charges $100, “for free.” Stone was soon able to persuade Seton to write off $297,000 of its $348,000 bill. Her argument was simple: There was no way the D.’s could pay it now or in the future, though they would scrape together $3,000 as a show of good faith. With the couple’s $3,000 on top of the $50,000 paid by the UnitedHealthcare insurance, that $297,000 write-off amounted to an 85% discount. According to its latest financial report, Seton applies so many discounts and write-offs to its chargemaster bills that it ends up with only about 18% of the revenue it bills for. That’s an average 82% discount, compared with an average discount of about 65% that I saw at the other hospitals whose bills were examined — except for the MD Anderson and Sloan-Kettering cancer centers, which collect about 50% of their chargemaster charges. Seton’s discounting practices may explain why it is the only hospital whose bills I looked at that actually reported a small operating loss — $5 million — on its last financial report.

Of course, had the D.’s not come across Stone, the incomprehensible but terrifying bills would have piled up in a box, and the Seton Medical Center bill collectors would not have been kept at bay. Robert Issai, the CEO of the Daughters of Charity Health System, which owns and runs Seton, refused through an e-mail from a public relations assistant to respond to requests for a comment on any aspect of his hospital’s billing or collections policies. Nor would he respond to repeated requests for a specific comment on the $24 charge for niacin pills, the $18 charge for the diabetes-test strips or the $77 charge for gauze pads. He also declined to respond when asked, via a follow-up e-mail, if the hospital thinks that sending patients who have just been told they are terminally ill bills that reflect chargemaster rates that the hospital doesn’t actually expect to be paid might unduly upset them during a particularly sensitive time. To begin to deal with all the other bills that kept coming after Steven’s first stay at Seton, Stone was also able to get him into a special high-risk insurance pool set up by the state of California. It helped but not much. The insurance premium was $1,000 a month, quite a burden on a family whose income was maybe $3,500 a month. And it had an annual payout limit of $75,000. The D.’s blew through that in about two months. The bills kept piling up. Sequoia Hospital — where Steven was an inpatient as well as an outpatient between the end of January and November following his initial stay at Seton — weighed in with 28 bills, all at chargemaster prices, including invoices for $99,000, $61,000 and $29,000. Doctor-run outpatient chemotherapy clinics wanted more than $85,000. One outside lab wanted $11,900.

|

| CT Scans Patient was charged $6,538 for three ct scans. Medicare would have paid a total of about $825 for all three |

Stone organized these and other bills into an elaborate spreadsheet — a ledger documenting how catastrophic illness in America unleashes its own mini-GDP.

In July, Stone figured out that Steven and Alice should qualify for Medicaid, which is called Medi-Cal in California. But there was a catch: Medicaid is the joint federal-state program directed at the poor that is often spoken of in the same breath as Medicare. Although most of the current national debate on entitlements is focused on Medicare, when Medicaid’s subsidiary program called Children’s Health Insurance, or CHIP, is counted, Medicaid actually covers more people: 56.2 million compared with 50.2 million. As Steven and Alice found out, Medicaid is also more vulnerable to cuts and conditions that limit coverage, probably for the same reason that most politicians and the press don’t pay the same attention to it that they do to Medicare: its constituents are the poor. The major difference in the two programs is that while Medicare’s rules are pretty much uniform across state lines, the states set the key rules for Medicaid because the state finances a big portion of the claims. According to Stone, Steven and Alice immediately ran into one of those rules. For people even with their modest income, the D.’s would have to pay $3,000 a month in medical bills before Medi-Cal would kick in. That amounted to most of Alice’s monthly take-home pay.

Medi-Cal was even willing to go back five months, to February, to cover the couple’s mountain of bills, but first they had to come up with $15,000. “We didn’t have anything close to that,” recalls Alice.

Stone then convinced Sequoia that if the hospital wanted to see any of the Medi-Cal money necessary to pay its bills (albeit at the big discount Medi-Cal would take), it should give Steven a “credit” for $15,000 — in other words, write it off. Sequoia agreed to do that for most of the bills. This was clearly a maneuver that Steven and Alice never could have navigated on their own. Covering most of the Sequoia debt was a huge relief, but there were still hundreds of thousands of dollars in bills left unpaid as Steven approached his end in the fall of 2011. Meantime, the bills kept coming. “We started talking about the cost of the chemo,” Alice recalls. “It was a source of tension between us … Finally,” she says, “the doctor told us that the next one scheduled might prolong his life a month, but it would be really painful. So he gave up.”